How would soaring property prices affect a 2024 Monopoly board?

Classic board game Monopoly hit shelves in 1935 and has been causing family arguments ever since. As the real estate game was loosely based on property values at the time it was launched it provides some interesting insights into how the market has changed over the last nine decades.

The original Monopoly game was based on Atlantic City, US, but it didn’t take long for the game to be adapted to new locations. Indeed, a London version of the game was available within months.

Since its launch, the game has sold more than 275 million copies worldwide and there are hundreds of different editions to choose from. So, if the game was updated to reflect 2024 prices, how would it be different?

Mayfair would continue to hold the top spot but prices have soared

Unsurprisingly, if you updated the property prices to reflect today’s figures, they would be much higher than they were in 1935, and some locations have fared better than others.

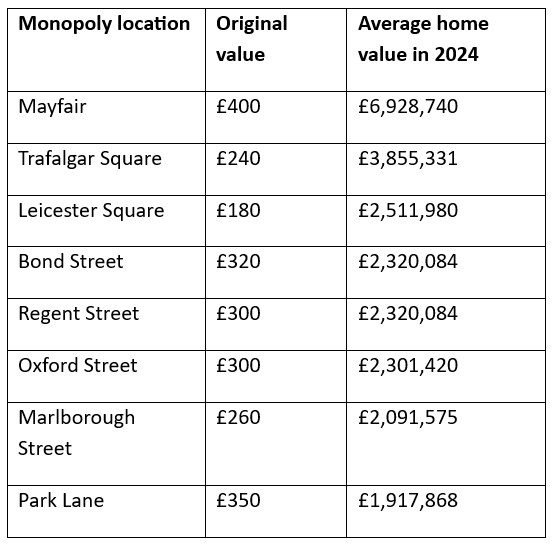

According to a report in IFA Magazine, using today’s prices, the top locations on the Monopoly board would be:

You might notice that the top properties don’t appear in the same order as they do on the board as some areas have seen prices rise far more rapidly than others.

In fact, the iconic dark blue set – the most expensive on the board – has changed. Mayfair continues to hold the top spot, with a value that’s significantly higher than other locations. However, Park Lane, once the second most expensive property, has fallen six places.

Even the cheapest properties on the board have seen huge increases in value.

Indeed, the first property on the board, Old Kent Road, was priced at an affordable £60. At today’s prices, a home on the same street would set you back around £342,000.

While property prices in London remain the highest in the UK, the trend is reflected across the country.

Land Registry data doesn’t go back to 1935, but the average property price in the UK was £3,595 in April 1968. By July 2024, the average price has increased to £289,723 – an increase of almost 8,000%.

Property prices have increased at a quicker pace than inflation

In the classic rules of Monopoly, you start with £1,500 and receive £200 every time you pass “GO”. According to the Bank of England, inflation would mean these figures rise to £89,644 and £11,952 respectively in August 2024.

Yet, they wouldn’t have the same spending power as rising property prices have outstripped average inflation over the last 90 years.

With your initial £1,500, you’d be able to buy several properties on the Monopoly board, even if you’re lucky enough to land on the more expensive tiles. Yet, with 2024 prices, you would still be some way short of being able to afford even the cheapest property – Old Kent Road at £342,000 – with your starting sum after it’s been adjusted for inflation.

Relying on the money you receive when passing GO would mean you’d need to go around the board more than 1,260 times to build up enough cash to buy Old Kent Road, which would be sure to lead to a long and tedious game.

The gap between rent and mortgage repayments is much closer

In Monopoly you make money and try to bankrupt others by charging players rent when they land on a tile you own.

Before you start adding houses and hotels to your tiles, the rent is usually half the purchase price. So, when you buy Old Kent Road for £60, you charge £30 rent. In reality, the cost of rent and mortgage repayments are far closer.

Indeed, according to Zoopla, between 2011 and 2022, renting a home was more expensive than paying a mortgage. Even with rising interest rates leading to mortgages becoming more expensive for the first time in 13 years, rent is only around 9.5% lower.

Contact us to talk about your mortgage

If you need a mortgage to buy your new home, whether the location is on the Monopoly board or not, we could help you find a lender that’s right for you and may be able to save you money. Please get in touch to talk about your needs.

Please note:

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

Your home may be repossessed if you do not keep up repayments on a mortgage or other loans secured on it.