Author: Richard Gross

Your Spring Statement update – the key news from the chancellor’s speech

After Rachel Reeves’ impactful first Budget in autumn 2024, you might have been concerned about the announcements that would be included in her Spring Statement on 26 March 2025.

Reassuringly, the major headline from this year’s springtime fiscal event is that Reeves made few announcements that are likely to affect you and your personal finances directly. Although, it did reveal that none of the changes made in the Autumn Budget would be overturned. However, one significant change has been made to the High Income Child Benefit Charge, which could affect you or your family.

The chancellor did announce that, due to global uncertainty and after the economy declined in January, the Office for Budget Responsibility (OBR) has downgraded its 2025 forecast for UK growth from 2% in October 2024 to 1% as of March 2025. She also noted the OBR’s long-term forecast, indicating that growth would increase for each year remaining in this parliament.

In addition to growth figures, the chancellor’s Statement introduced a range of measures designed to increase economic activity in the UK, as well as cost-saving initiatives, predominantly at state level, to reduce government debt.

Read on for your summary of the chancellor’s 2025 Spring Statement.

Personal tax thresholds and allowances are set to remain unchanged

Those who were concerned the chancellor would announce sweeping changes that might affect their personal finances will be breathing a sigh of relief as many worries didn’t materialise.

Personal tax

Reeves stuck to a pre-Spring Statement commitment to not increase personal taxes.

So, Income Tax thresholds and rates will remain unchanged, and thresholds are frozen until April 2028. As a result, your Income Tax liability is likely to rise in real terms.

Similarly, the rates and thresholds for paying Capital Gains Tax (CGT) and Dividend Tax will remain the same.

Individual Savings Accounts (ISAs)

Before the Spring Statement, the government was reportedly considering reducing the amount you can tax-efficiently place in a Cash ISA each tax year to £4,000 in a bid to encourage greater investment.

The good news is the ISA subscription limit will remain at the current level (£20,000) in the 2025/26 tax year. The ISA subscription limit is frozen until 2030.

The Junior ISA (JISA) allowance will remain at £9,000 in 2025/26.

However, the government did note it will continue reviewing ISA reform options to improve the balance between cash and equities to earn better returns for savers, boost the culture of retail investment, and support its growth mission.

Pensions

Last year, the government announced a new Pension Schemes Bill, which will legislate several areas of pension policy. However, further reforms weren’t announced in the Spring Statement.

The Annual Allowance will remain at £60,000 in 2025/26. Your Annual Allowance may be lower if your income exceeds certain thresholds or you have already flexibly accessed your pension.

As usual, there was also speculation that the amount you could withdraw from your pension tax-free would be reduced, but this has remained unchanged. So, when you reach the normal minimum pension age (55, rising to 57 in 2028), you may withdraw up to 25% of your pension (up to a maximum of £268,275) before paying Income Tax.

State Pension

As expected, there were no announcements relating to the State Pension or the triple lock, which guarantees the State Pension will increase every tax year by either the rate of inflation, average earnings growth, or 2.5%, whichever is higher.

As a result, the full new State Pension will pay a weekly income of £230.25 in 2025/26.

High Income Child Benefit Charge reforms will come into place this summer

Although the chancellor did not explicitly announce the change, the Spring Statement document revealed that those who pay the High Income Child Benefit Charge will be able to do so through PAYE from summer 2025.

As it stands, those who pay the charge need to register for self-assessment to do so, even if they do not otherwise need to self-assess. But this year, the government is making it easier for families to pay the charge without needing to submit a tax return.

Inflation is forecast to meet the Bank of England’s 2% target by 2027

After reaching a 40-year high of 11.1% in October 2022, inflation, as measured by the Consumer Prices Index (CPI), has gradually fallen, bringing it closer to the Bank of England’s (BoE) target of 2%.

The chancellor announced in her Statement that in the 12 months to February 2025, inflation rose by 2.8%, down from 3% in January. Now that inflation is better under control, the BoE has cut its base rate three times since the general election, bringing the rate down from 5.25% to 4.5%. These cuts mean borrowers will likely pay less while savers may see their interest payments fall.

It was then announced that, according to the OBR’s forecast, inflation will average:

- 3.2% in 2025

- 2.1% in 2026

- 2% in 2027, 2028, and 2029 – the BoE’s target rate.

The key fiscal announcements from the 2025 Spring Statement

The chancellor’s speech largely revolved around changes to government spending and investment. Some of the key measures and announcements included in the Statement were to:

- Increase defence spending to 2.5% of GDP by 2027, including providing an additional £2.2 billion to the Ministry of Defence next year

- Rebalance payment levels in Universal Credit to incentivise people into work, and review the assessment for Personal Independence Payments, with the OBR stating these changes will save £4.8 billion from the welfare budget in 2029/30

- Crack down on promoters of tax avoidance schemes, as initially announced in the Autumn Budget in October 2024

- Invest £2 billion in social and affordable housing, so housebuilding reaches a 40-year high that helps put the government on track to reach its target of building 1.5 million homes by the end of this parliament

- Introduce a £3.25 billion Transformation Fund to streamline public services using technology and Artificial Intelligence, making the government “leaner and more efficient”. Additionally, government departments will reduce their administrative budgets by 15% by the end of the decade.

2024 Autumn Budget changes remain intact

In October 2024, the chancellor announced a series of tax-raising measures during the Autumn Budget, some of which could have affected your personal finances. These included:

- Inheritance Tax (IHT) will be levied on unused pension benefits from April 2027.

- Agricultural Property Relief and Business Property Relief will be reduced from April 2026.

- CGT rates for non-property gains were raised in line with property rates with immediate effect, and Business Asset Disposal Relief and Investors’ Relief were both reduced.

- Employer National Insurance contributions (NICs) will rise from April 2025, from 13.8% to 15%, and the threshold at which employers start paying NICs will also fall.

- Income Tax thresholds will remain frozen until 2028.

- The IHT nil-rate bands will remain fixed for a further two years, until 2030.

- VAT was levied on fee-paying schools, effective from 1 January 2025.

- The non-dom tax regime is set to be abolished from April 2025.

- The Stamp Duty Land Tax surcharge on second home purchases rose from 3% to 5% from 31 October 2024.

- Corporation Tax is now capped at 25% for the duration of the parliament.

While many hoped the chancellor would row back on some or all of these measures, all remain intact.

Please note

All information is from the Spring Statement documents on this page.

The content of this Spring Statement summary is intended for general information purposes only. The content should not be relied upon in its entirety and shall not be deemed to be or constitute advice.

While we believe this interpretation to be correct, it cannot be guaranteed and we cannot accept any responsibility for any action taken or refrained from being taken as a result of the information contained within this summary. Please obtain professional advice before entering into or altering any new arrangement.

Investment market update: December 2024

Political instability in Europe and further afield affected investment markets in December. Read on to find out what other factors may have influenced your investment returns at the end of 2024.

Remember to focus on your long-term goals when assessing the performance of your investments. The value of your assets rising and falling is part of investing. What’s important is that the risk profile is appropriate for you and that your decisions align with your circumstances and aspirations.

UK

Hopes that the Bank of England (BoE) would cut its base interest rate before the end of 2024 were dashed when data showed inflation had increased.

Figures from the Office for National Statistics show inflation was 2.6% in the 12 months to November 2024, which was up from the 2.3% recorded a month earlier.

This led to the BoE deciding to hold interest rates despite speculation that a cut was on the horizon. The central bank also said it expects GDP growth to be weaker at the end of 2024 than it had previously predicted.

Data paints a gloomy picture for the manufacturing sector.

According to S&P Global’s Purchasing Managers’ Index (PMI), UK manufacturing hit a nine-month low as output fell for the first time in seven months in November 2024. The decline was driven by new orders falling. Notably, manufacturers are struggling to export their goods, with new orders contracting for 31 consecutive months. Demand has fallen in key markets, including the US, China, the EU, and Middle East.

A survey from the Confederation of British Industry (CBI) indicates that manufacturers aren’t optimistic about the future either. The organisation said orders at UK factories “collapsed” in December to their lowest level since the height of the pandemic in 2020. The slump was linked to political instability in some European markets and uncertainty over US trade policy when Donald Trump becomes president.

Chancellor Rachel Reeves wants to reduce UK trade barriers with the US, stating she wanted to end the “fractious” post-Brexit accord as she went to meet eurozone finance ministers at the start of the month. Closer ties with the EU may benefit some firms that are struggling with exports.

Retailers are also experiencing challenges.

The festive period is often crucial for retailers. Yet, data from Rendle Intelligence and Insights are “bleak” with footfall in the first two weeks of December down 3.1% when compared to 2023. A slew of high street names entered administration in 2024, including Homebase, The Body Shop, and Ted Baker, and the research suggests more could follow suit in the year ahead.

December was a month of ups and downs for investors in the UK stock market.

The month started strong when stock markets increased across Europe on 3 December – dubbed a “Santa rally” in the media. The FTSE 100 – an index of the 100 largest firms on the London Stock Exchange – was up 0.7% despite worries about the economic outlook. EasyJet led the way with a 4% boost.

Yet, just mere weeks later, on 17 December, the FTSE 100 hit a three-week low and lost 0.7%. The biggest faller was Bunzl, a distribution and outsourcing company, which fell 4.6% when it warned persistent deflation would weigh on profits in 2024.

While it might have felt like a bumpy year as an investor, research shows the FTSE 100 has performed well. Indeed, according to AJ Bell, the index had its best year since 2021 and delivered a return of 11.4%. The top performers were NatWest and Rolls-Royce, while JD Sports and B&M were at the bottom of the pack.

Europe

Much like the UK, the manufacturing sector in the eurozone is struggling. Indeed, PMI data shows the sector continued to contract in November 2024 as new factory orders fell. Germany recorded the fastest drop in output and, as the bloc’s largest economy, could drag economic data down.

Dr Cyrus de la Rubia, chief economist at Hamburg Commercial Bank, told the Guardian: “These numbers look terrible. It’s like the eurozone’s manufacturing recession is never going to end.”

Credit ratings firm Moody’s unexpectedly downgraded French government bonds, which are now rated Aa3 – the fourth highest rating – following the collapse of Michel Barnier’s government. MPs had refused to accept tax hikes and spending cuts in Barnier’s Budget.

Moody’s said: “Looking ahead, there is now very low probability that the next government will sustainably reduce the size of fiscal deficits beyond next year. As a result, we forecast that France’s public finances will be materially weaker over the next three years compared to our October 2024 baseline scenario.”

The news, unsurprisingly, led to French bonds weakening.

European markets also benefited from the so-called Santa rally on 3 December.

Germany’s DAX, a stock index of the 30 largest German companies on the Frankfurt Exchange, broke the 20,000-point barrier for the first time, despite a new election being called after the government collapsed. The recent boost means the DAX increased by around 3,000 points during 2024.

Similarly, Paris’s stock market index, the CAC, gained 0.6%. Luxury goods makers, like Hermes and LVMH, were among the biggest risers.

US

Unlike Europe, US manufacturing could give investors something to be optimistic about.

The PMI reading for November 2024 was 49.7, up from 48.5. While this means the sector is still below the 50-mark indicating growth, the signs suggest it’s stabilising and could move into more positive territory in the new year.

The service sector paints an even better picture. The PMI indicated the sector is growing at its fastest pace since the Covid-19 pandemic. Expectations of higher output linked to growing optimism about business conditions under the Trump administration led to a flash PMI reading of 56.6 for December, comfortably placing the sector in growth territory.

The job market also bounced back after disappointing figures in October. According to the US Bureau of Labor Statistics, 227,000 jobs were added to the economy in November, compared to just 36,000 a month earlier.

Yet, inflation continues to weigh on the US. In the 12 months to November 2024, inflation increased slightly to 2.7%.

While the Federal Reserve went ahead with an interest rate cut, taking the base rate to 4.25%, it also suggested it would make fewer cuts than expected in 2025 if inflation remains stubborn. The comments led to the S&P 500 index closing almost 3% down, while the tech-focused Nasdaq fell 3.6% on 19 December.

President-elect Trump is set to take office on 20 January 2025, but his plans are already influencing markets. Indeed, on 2 December, the dollar rallied after Trump warned countries in the BRICS bloc that he would impose 100% tariffs if they challenged the US dollar by creating a new rival currency.

The BRICS bloc was originally composed of Brazil, Russia, India, China, and South Africa, which led to the acronym. They have since been joined by Iran, Egypt, Ethiopia, Saudi Arabia and the United Arab Emirates.

Asia

In a move that shocked citizens, South Korea’s president declared martial law on 3 December, which led to political chaos. The uncertainty led to South Korea’s currency dropping to a two-year low and exchange-traded funds (ETFs), which track the country’s shares, fell sharply. Indeed, the MSCI South Korea EFT dropped by more than 5% in the immediate aftermath.

Outside of South Korea, stock market performances were more positive in Asia.

On 9 December, Hong Kong’s Hang Seng was up by 2% after China said it would implement a more proactive fiscal policy and planned to loosen monetary policy in 2025. The market was also aided by consumer inflation in China falling to a five-month low in November to 0.2%.

On the same day, Japan revised its economic growth upwards, leading to a 0.3% boost to the Nikkei 225 index.

Please note:

This blog is for general information only and does not constitute financial advice, which should be based on your individual circumstances. The information is aimed at retail clients only.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

3 insightful property market predictions for 2025

Key changes, like interest rates falling and Stamp Duty thresholds changing, are likely to affect the property market in 2025.

Whether you’re buying, selling, or simply interested in how the value of your home might change over the next 12 months, read on to discover three insightful property market predictions for the year ahead.

1. Stamp Duty changes are expected to boost property transactions at the start of the year

In the Autumn Budget, chancellor Rachel Reeves announced the temporary higher thresholds for paying Stamp Duty would end in April 2025.

Stamp Duty is a type of tax you pay when you purchase property or land. The higher threshold has meant many families have benefited from paying a lower rate or even avoiding the tax completely. With the threshold lowering in April 2025, the number of property transactions concluded during the first quarter of the year is expected to be high.

In fact, Zoopla predicts there will be a 5% increase in sales across 2025 to 1.15 million.

One of the key reasons driving this boost is the changes to Stamp Duty, which will encourage first-time buyers and home movers to purchase property before the deadline.

It could be good news for sellers, as you may find interest in your property rises and buyers are more motivated to complete transactions quickly.

2. Interest rates are predicted to fall but at a slower pace than earlier forecasts

When inflation was high, the Bank of England (BoE) increased its base interest rate throughout 2022 and 2023 in a bid to slow it down.

For many families with a mortgage, this meant their mortgage repayments increased. In 2024, the central bank started to reduce the interest rate as inflation stabilised. As of December 2024, the base interest rate was 4.75%.

Previously, many experts were predicting the BoE would make regular cuts to the base interest rate toward the end of 2024 and throughout 2025.

However, statistics from the Office for National Statistics (ONS) show the rate of inflation increased in the 12 months to November 2024 to 2.6%, compared to 2.3% a month earlier. This partly led to the BoE choosing to hold the base interest rate in December 2024.

So, will interest rates fall in 2025 as predicted?

It’s good news for mortgage holders as many experts still agree that interest rates will fall in 2025, but perhaps at a slower pace than earlier predictions suggested.

Indeed, according to MoneyWeek, BoE governor Andrew Bailey suggested the bank could cut interest rates four times in 2025. Recently, when changing the base rate, the bank has made an increase or decrease of 25 basis points. If it continued to follow this pattern, that would lead to an interest rate of 3.75% by the end of 2025.

3. Improving conditions for households could lead to property prices rising

Interest rates falling would make mortgage repayments more affordable for many families. In turn, this could lead to property prices rising.

In addition, strong wage growth could support the market too. According to the ONS, annual growth in employee’s average earnings was 5.2% for the period from August to October 2024. With wages now growing at a faster pace than inflation, more families might feel financially secure enough to move up the property ladder or aspiring homeowners could find they’re now in a better position to secure a mortgage.

Property firm Savills now predicts that property prices will rise by 3.5% in 2025, leading to an average property price of £302,500. It expects the boom to continue over the next few years too.

Between 2024 and 2028, it predicts that property prices will increase by 21.6%, leading to an average property price of £346,500 by the end of the forecast period.

Will you be taking out a mortgage in 2025?

If you’ll be taking out a new mortgage deal in 2025, we could help you find one that’s right for you. Whether you’re moving home or your current deal is set to expire, finding a competitive deal could save you money.

Get in touch with us to find out how we may help you find a mortgage.

Please note:

This blog is for general information only and does not constitute financial advice, which should be based on your individual circumstances. The information is aimed at retail clients only.

Your home may be repossessed if you do not keep up repayments on a mortgage or other loans secured on it.

Fiscal drag: How threshold and allowance freezes affect you

Despite intense speculation that the Labour government would slash tax allowances and exemptions, many are set to remain the same in the 2025/26 tax year. While that might seem like something to celebrate, fiscal drag could mean your tax liability increases in real terms.

To maintain allowances and exemptions in real terms, the government would need to increase them by the rate of inflation.

So, when they are frozen instead, your taxable income is likely to increase as you might be “dragged” into paying tax or paying tax at a higher rate. This generates higher revenues for the government without increasing tax rates. For this reason, freezes are sometimes called “stealth taxes”.

Several tax thresholds have been frozen since April 2022 and aren’t expected to rise until April 2028. When you consider the period of high inflation experienced recently, the effect of fiscal drag could mean you’ve paid a significantly higher proportion of tax, relative to your income, than you did previously.

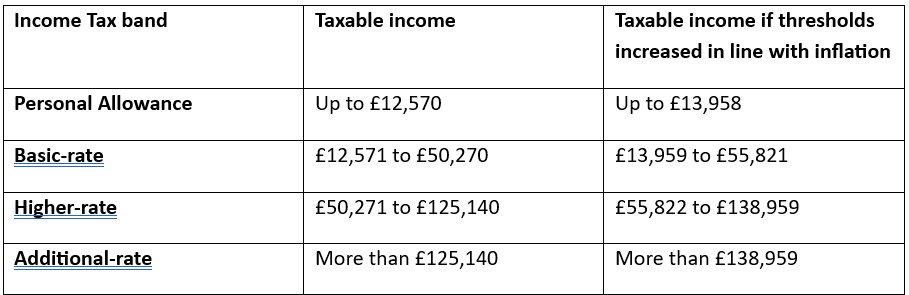

Income Tax: Thresholds are frozen until April 2028

The previous Conservative government froze Income Tax thresholds in 2022 until April 2028. The current Labour government has said it will continue the freeze.

During the freeze, it’s likely that your income will rise, which would maintain your spending power. However, as the thresholds will not increase, your tax liability might also rise. It may seem like a small increase initially, but it can add up over the years.

The table below shows how the value of Income Tax thresholds would have changed if they had increased in line with inflation between January 2022 and November 2024.

Source: Bank of England

With the freeze expected to remain in place for another three years, the effects of fiscal drag will become more evident.

According to the Office of Budget Responsibility (OBR), freezing Income Tax thresholds mean that between 2022/23 and 2028/29, an extra 4 million people will pay Income Tax. In addition, 3 million will be dragged into the higher-rate tax band and 400,000 will pay the additional-rate of Income Tax for the first time.

The fiscal drag is estimated to raise £42.9 billion in tax by 2027/28.

The OBR noted frozen thresholds are the largest contributor to the rising overall economy-wide tax burden. The freeze will be responsible for almost a third of the 4.5% GDP increase in taxes from 2019/20 to 2028/29.

Freezes to Inheritance Tax thresholds and ISA limits could affect your finances too

It’s not just freezes to Income Tax you may need to be mindful of either. Frozen allowances include the:

- Inheritance Tax thresholds: The nil-rate band is frozen at £325,000 – it has been at this level since 2009/10 and will remain the same until April 2028. The residence nil-rate band last increased to £175,000 in 2020/21 and is also frozen until the start of the 2028/29 tax year.

- ISA allowance: The amount you can add to your ISA each tax year is frozen at £20,000 for adults and £9,000 for children until 5 April 2030. The amount you can pay into an adult ISA hasn’t increased since 2018/19, and the Junior ISA subscription limit last increased in 2020/21.

There are other allowances and exemptions that, while not frozen, haven’t increased in line with inflation either.

For example, the amount you can gift in a tax year that will be immediately outside of your estate for Inheritance Tax purposes is known as the “annual exemption”. In 2024/25, the annual exemption is £3,000 and it’s been at this level since 1981.

If the annual exemption had increased in line with inflation between 1981 and November 2024, it’d stand at £11,314.

A financial plan could help you minimise the effects of fiscal drag

While you can’t change tax thresholds or allowances, there might be steps you can incorporate into your financial plan to reduce your overall tax bill.

For instance, increasing your pension contributions could reduce your taxable income and mean you avoid being dragged into a higher Income Tax bracket. While it may mean your take-home pay is lower, it could support long-term retirement goals and may be right for you as a result.

In addition, while the ISA allowance is frozen, if you’re not already depositing the full amount, increasing how much you add to your ISA may reduce your Income Tax bill.

Interest earned on savings that aren’t held in a tax-efficient wrapper, like an ISA, could become liable for Income Tax if they exceed your Personal Savings Allowance (PSA). The PSA is £1,000 if you’re a basic-rate taxpayer, £500 if you’re a higher-rate taxpayer, and £0 if you’re an additional-rate taxpayer.

If you’d like to talk about how fiscal drag may affect your finances and the steps you might take to mitigate the effects, please get in touch.

Please note:

This blog is for general information only and does not constitute financial advice, which should be based on your individual circumstances. The information is aimed at retail clients only.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

5 useful allowances and exemptions that will reset at the end of the tax year

Using allowances and exemptions could reduce your overall tax bill and help you get more out of your money. On 5 April 2025, the current tax year will end, and many tax-efficient allowances and exemptions will reset. So, here are five that you may want to consider using before the 2025/26 tax year starts.

1. ISA allowance

ISAs provide a popular way to tax-efficiently save and invest. Indeed, the latest government figures show in 2022/23, 12.4 million ISAs were subscribed to with around £71.6 billion being collectively added to accounts.

For the 2024/25 tax year, you can add up to £20,000 to ISAs. If you hold money in a Cash ISA, the interest you receive wouldn’t be liable for Income Tax. Similarly, if you invest through a Stocks and Shares ISA, any returns generated aren’t liable for Capital Gains Tax (CGT).

If you don’t use your ISA allowance before the tax year ends, you’ll lose it. So, it could be worthwhile reviewing your saving and investing goals now.

Before you place money into an ISA, it’s often a good idea to consider your goal. For short-term goals, a Cash ISA might be suitable for your needs. On the other hand, if you’re putting money away for a goal that’s more than five years away, you may want to consider if you could benefit from investing.

In addition, if you’re aged between 18 and 39, you could open a Lifetime ISA (LISA). In the 2024/25 tax year, you can add up to £4,000 to a LISA and receive a 25% government bonus. The £4,000 LISA allowance counts towards your overall £20,000 ISA allowance.

However, if you withdraw money from a LISA before the age of 60 for a purpose other than buying your first home, you’d pay a 25% penalty. As a result, a LISA is often most suitable for those saving to get on the property ladder.

2. Dividend Allowance

If you’re a business owner or hold shares in some companies, you might receive dividends.

You don’t pay tax on dividends that fall within your Personal Allowance, which is £12,570 in 2024/25. In addition, you can receive up to £500 in dividends before Dividend Tax is due under your Dividend Allowance. So, dividends could offer a valuable way to boost your income without increasing your tax liability.

You cannot carry forward unused Dividend Allowance.

Even if your dividends could exceed the allowance, the tax rate you pay could be lower than receiving a comparable amount that was liable for Income Tax. The rate of Dividend Tax you pay depends on your Income Tax band. In 2024/25, the rates are:

- Basic rate: 8.75%

- Higher rate: 33.75%

- Additional rate: 39.35%

So, making dividends part of your financial plan could reduce your overall tax bill even if you’re liable for Dividend Tax.

3. Capital Gains Tax Annual Exempt Amount

Chancellor Rachel Reeves made several changes to CGT in the Autumn Budget, including increasing the main rates. Consequently, you could find your tax liability is higher than expected when you make a profit when you dispose of some assets.

Indeed, the Office for Budget Responsibility estimates CGT could raise £15.2 billion in 2024/25, which may then increase to £23.5 billion in 2028/29.

From 30 October 2024, the standard rates of CGT are:

- 24% if you’re a higher- or additional-rate taxpayer

- 18% if you’re a basic-rate taxpayer and the gains fall within the basic-rate Income Tax band.

Importantly, the Annual Exempt Amount means you can make profits of up to £3,000 in 2024/25 before CGT is due. So, if you plan to dispose of assets, timing the decision to make use of this exemption could be valuable.

You cannot carry forward the Annual Exempt Amount into the new tax year if you don’t use it.

4. Pension Annual Allowance

Pensions provide a tax-efficient way to save for your retirement as contributions benefit from tax relief and the interest or investment returns generated are tax-free.

In 2024/25, the Pension Annual Allowance is £60,000 – this is the amount you can tax-efficiently add to your pension in a single tax year, so you might also need to consider employer contributions and those made by other third parties. However, you can only claim tax relief on up to 100% of your annual earnings, or £2,880 if you’re a non-taxpayer.

There are two reasons why your Annual Allowance may be lower.

- If your adjusted income is more than £260,000 and your threshold income is more than £200,000, the allowance will taper. For every £2 your income exceeds the adjusted income threshold, your Annual Allowance will fall by £1. The tapering stops at £360,000, so everyone retains an allowance of £10,000.

- If you’ve already flexibly accessed your pension, the Money Purchase Annual Allowance may affect you. This reduces the amount you can tax-efficiently add to your pension to £10,000.

You can carry your Annual Allowance forward for up to three tax years. So, you have until 5 April 2025 to use any unused allowance from 2021/22.

5. Inheritance Tax annual exemption

Government figures suggest Inheritance Tax (IHT) bills are on the rise. Indeed, IHT tax receipts between April 2024 and October 2024 were £5 billion – around £500 million higher than the same period last year.

If your estate could be liable for IHT when you die, passing on wealth during your lifetime could be a valuable way to reduce a potential bill.

However, not all gifts are considered immediately outside of your estate for IHT purposes. Some may be included in your estate for up to seven years, which are known as “potentially exempt transfers”.

So, using allowances and exemptions that enable you to pass gifts to your loved ones without worrying about IHT might be an important part of your estate plan.

In 2024/25, the annual exemption means you can pass on £3,000 without worrying about IHT. You can carry forward your annual gifting exemption from the previous tax year, so you could gift up to £6,000 in a single tax year and have it fall immediately outside your estate.

There are often other allowances or ways you could reduce your estate’s potential IHT bill. Please contact us to talk about steps you may take.

Get in touch to discuss your end-of-year tax plan

If you’d like to talk about which allowances and exemptions you may want to use to reduce your tax bill in 2024/25, please get in touch. We’ll work with you to help you understand which steps could be right for your circumstances and aspirations.

Please note:

This blog is for general information only and does not constitute financial advice, which should be based on your individual circumstances. The information is aimed at retail clients only.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.

The Financial Conduct Authority does not regulate tax planning, Inheritance Tax planning, or estate planning.

Plans changed? Updating your financial plan could offer reassurance

Even the best-laid financial plan might need to change at times. If you find yourself in that position, you might benefit from reassurance that you can still reach your goals and will be financially secure.

There’s a whole host of reasons why you might want to adjust your financial plan.

In some cases, it might be a decision you’ve made. Perhaps you’ve decided you want to gift money to loved ones to help them reach their goals, or you want to take a higher income from your pension to fund a new-found hobby.

Other times, the changes might be due to factors outside of your control. For example, if you’ve been made redundant, you might need to create an income until you can find a new position.

Whatever the reason, it can be scary to change course. One cause of apprehension might be the fear of the unknown. Fortunately, updating your financial plan could help you feel more in control and confident.

Updating your cashflow model could help you analyse the impact of the changes

When you create a financial plan, one useful tool that you might use is a cashflow model.

You start by inputting some basic financial information into the model. For example, you might add the value of the assets you hold now, your income, and your outgoings.

One of the key benefits of a cashflow model is that it can help you visualise how your wealth might change over time.

So, you need to provide information to allow it to create a forecast too. This data often falls into two categories:

- Your actions – These would be the financial steps you plan to take, such as how much you plan to contribute to your pension each month or the amount you’ll add to an emergency fund.

- Assumptions – Some factors that might affect your finances are outside of your control, so for these areas, you may make realistic assumptions. For example, you might review your pension and include average annual returns of 5%.

With these details, a cashflow model can project how your assets and wealth may change and even look decades ahead so you can consider long-term goals.

As a result, cashflow modelling can help you understand if the steps you’re taking now are enough to secure the future you want. But it’s not just useful when everything is going to plan, a cashflow model may be even more valuable when you face unexpected changes.

It’s important to note that the projections from a cashflow model cannot be guaranteed. However, it can provide a useful indicator and highlight where there could be potential gaps in your financial plan.

A cashflow model could help you assess the short- and long-term impact of your new plans

So, you’ve worked with a financial planner and created a cashflow model that aligned with your aspirations. But now, your plans have been derailed. Luckily, you can update the information and model your new circumstances or goals.

Let’s say you’d previously planned to retire at the age of 65. However, ill health has forced you to step back from work five years sooner than you expected. You might have questions like:

- Can I afford to take an income from my pension in line with my previous plan?

- If I had to take a lower income, how would it affect my lifestyle?

- Are there other assets I could use to supplement an income from my pension?

- Could retiring sooner affect the value of the estate I leave behind for loved ones?

You can alter the information that goes into your cashflow model to help you answer these questions. So, in the above scenario, you might see how taking the same income you’d previously planned but five years earlier affects your risk of running out of money during your lifetime.

You might find that you have enough to be financially secure and can move forward with your retirement plans.

Alternatively, you may find that your new plan might leave you in a financially vulnerable position in the future. In this case, you can use the cashflow model to try different solutions to understand what might work for you.

By realising there’s a potential shortfall sooner, you’re in a better position to bridge gaps or find a different option, so you’re able to proceed with confidence.

Get in touch to update your financial plan

If your circumstances or goals have changed, you can arrange a meeting with our team to update your financial plan. It could help you assess the potential long-term implications of the changes and understand what steps you might need to take to keep your plan on track.

Please note:

This blog is for general information only and does not constitute financial advice, which should be based on your individual circumstances. The information is aimed at retail clients only.

The Financial Conduct Authority does not regulate cashflow modelling.

Why building emotional resilience could improve your finances

Emotions can affect how you feel about different scenarios and your response to them, including when you’re making financial decisions. Improving your emotional resilience could mean you’re better equipped to handle stressful situations. Read on to discover why and how it might support your financial goals.

Emotional resilience simply refers to your ability to adapt to and deal with stressful situations. It could help you remain level-headed even when you’re facing challenges.

It’s not about repressing your emotions, but recognising them and not letting them rule your decisions. As a result, it may be a valuable skill in your day-to-day life as well as when you’re managing your finances.

Here are five ways you could improve your emotional resilience.

1. Give what you do a meaning

Giving your actions a meaning could be hugely valuable. Indeed, a purpose could improve your resilience and mean you make better lifestyle choices.

Day-to-day that might mean finding a purpose in your work or social life. For instance, what motivates you to work, or what brings you joy in your free time?

When it comes to your finances, you can give your decisions a purpose too. When you’re setting money aside having a goal could mean you’re more motivated.

For instance, while you might make a pension contribution each month, it’s easy to feel disconnected from your retirement savings as the milestone could be decades away. So, taking some time to understand how these contributions will add up and what it could mean for your future might be useful. It may also mean you’re less likely to act on potentially harmful emotions, such as selecting a low-risk approach to investing because you’re worried, even if your circumstances mean more risk could be appropriate.

2. Focus on the positive

When you’re faced with a challenge, it can be easy to overlook the positives in a situation. Someone who is emotionally resilient is more likely to look for the silver lining even while acknowledging there are negatives.

It’s a strategy that could help stressful situations feel more manageable and mean that you’re in a better mindset to tackle what you need to do or make decisions. Next time you’re experiencing negative emotions like stress or worry, try to look on the bright side.

3. Be self-aware

One of the biggest challenges of managing your emotions is recognising when they could be harming your approach to the situation.

Being self-aware and understanding the effect your emotions are having could help you rein them in when appropriate. Asking yourself questions in the moment could help you reassess situations and come up with a solution that’s right for you.

So, trying to be more self-aware could be useful. There are many different ways to do this. You might find that when your emotions are heightened, taking a quick break from a task or decision gives you the space you need to become more level-headed. Some people find that keeping a journal provides them with a great opportunity to reflect on their day and recognise patterns.

4. Discover how to regain your sense of calm

Even with emotional resilience, there will be times when emotions like stress and fear will affect you.

Knowing what steps you can take to regain your sense of calm and feel in control again could be immensely useful. There’s not a single solution to lowering your blood pressure, so try different activities and find something that works for you. Some might find that quietly reading a book puts them at ease, while, for others, getting active is the perfect way to beat stress.

It could mean next time you feel that emotions might be affecting your decisions, you know what steps to take to regain your sense of calm.

5. Have someone you can turn to

When you’re struggling with emotions, having the right support network around you could make all the difference.

Having someone listen to you might help you keep your emotions in check. In your day-to-day life, those people might be your family, friends, or colleagues. They could also be a valuable source of support when you’re facing challenges around financial decisions.

In addition, your financial planner may also be someone you want to turn to in these circumstances. As they understand your financial position and goals, they could offer tailored advice that helps you assess situations with your circumstances in mind and formulate a plan that suits your needs.

If you’d like to talk to one of our team about your financial plan, please get in touch.

Please note:

This blog is for general information only and does not constitute financial advice, which should be based on your individual circumstances. The information is aimed at retail clients only.

Guide: The surprising benefits of choosing a “living legacy” for your loved ones

Leaving wealth behind for your loved ones may be a priority when developing your financial plan. After all, you’ll likely want to see your family thrive and an inheritance could help them achieve important goals in life.

Traditionally, you would transfer wealth to your loved ones when you passed away, leaving instructions in your will about how your family should divide your estate.

However, in recent years, more people have chosen to instead leave a “living legacy” – passing wealth to their loved ones while they’re still alive.

This informative guide explains why a living legacy could help you:

- Encourage your beneficiaries to think about their long-term finances

- Lend a helping hand to loved ones when they need it most

- Reduce a potential Inheritance Tax bill on your estate

- Offer valuable support around how to use the wealth.

As well as the potential benefits, this guide also considers the downsides you might need to consider, such as making estate planning more complex and balancing gifts with your own long-term financial security.

Download your copy here: ‘The surprising benefits of choosing a “living legacy” for your loved ones’ to find out more now.

If you want to discuss ways to pass wealth to your loved ones while ensuring that you can meet your own financial goals, please contact us to arrange a meeting.

Your Autumn Budget update – the key news from the chancellor’s statement

Almost four months after Labour won the general election, chancellor Rachel Reeves has delivered her 2024 Autumn Budget, outlining the government’s plans for this tax year and beyond.

Arguing that the July general election had given Labour a “mandate to restore stability and start a decade of renewal”, Reeves described it as “a Budget to fix the foundations and deliver change”.

Against a backdrop of a manifesto pledge not to increase Income Tax, employee National Insurance, or VAT, Reeves also announced that her Budget would raise taxes by £40 billion, stating that any other chancellor would “face the same reality”.

Read on for a summary of some of the key measures and announcements from this year’s Autumn Budget – the first ever delivered by a woman – and what they might mean for you.

Extra investment in infrastructure

The chancellor argued that “the only way to drive economic growth is to invest, invest, invest.”

In the run-up to the Budget, Reeves announced she was making a technical change to the way debt is measured, which will allow the government to fund extra investment. This wider debt measure will allow for more borrowing to invest in big building projects such as roads, railways, and hospitals.

It’s important to note that this additional room for manoeuvre for spending on investment projects will not be used to support day-to-day spending, as the chancellor has committed to fund that with tax receipts.

A rise in employer National Insurance contributions

As many analysts had predicted, Reeves increased employer National Insurance (NI) rates by 1.2% from 13.8% to 15%, effective 6 April 2025.

Currently, employers pay NI only above a threshold of £9,100 a year. The chancellor reduced this threshold to £5,000 a year, effective 6 April 2025. The threshold will remain at £5,000 until 6 April 2028 and then increase in line with the Consumer Prices Index (CPI) thereafter.

These reforms will raise £25 billion a year by the end of the forecast period (2029/30).

At the same time, the government is increasing the Employment Allowance.

The current Employment Allowance gives employers with NI bills of £100,000 or less a discount of £5,000 on their employer NI bill.

From 2025, the Employment Allowance will rise to £10,500. Moreover, the government will expand the Employment Allowance by removing the £100,000 eligibility threshold so that all eligible employers now benefit.

Taken together, the government says that 865,000 businesses will pay no NI contributions at all, and more than half of employers with NI liabilities will either see no change or will gain overall next year.

An end to the freeze on Income Tax thresholds from 2028

Back in 2021, the then-chancellor, Rishi Sunak, raised both the Personal Allowance and the threshold at which higher-rate Income Tax is due by £70 and £270 respectively.

Importantly, however, he also fixed these thresholds until 2026. Then, in the 2022 Autumn Statement, Jeremy Hunt extended this freeze until 2028.

Unexpectedly, Reeves decided against extending the freeze beyond 2028. From 2028/29, personal tax thresholds will be uprated in line with inflation once again.

Capital Gains Tax reforms

The chancellor announced several changes to the Capital Gains Tax (CGT) regime.

Firstly, as of 30 October, the main rates of CGT have increased. The basic rate has risen from 10% to 18% and the higher rate has increased from 20% to 24%.

The government will maintain the lifetime limit for Business Asset Disposal Relief (BADR) – formerly Entrepreneurs’ Relief – at £1 million. Meanwhile, the lifetime limit for Investors’ Relief (IR) will be reduced from £10 million to £1 million.

The BADR and IR rate of CGT will continue to be charged at 10%, before rising to 14% on 6 April 2025 and 18% on 6 April 2026.

These measures will raise £2.5 billion a year by the end of the forecast period.

Furthermore, CGT on carried interest – paid by private equity managers – will rise from 18% (basic rate) and 28% (higher rate) to 32% from 6 April 2025. There will be further reforms from April 2026 to bring carried interest within the Income Tax framework, under bespoke rules.

Changes to some Inheritance Tax reliefs

As expected, the chancellor made key announcements that could affect estate planning.

Nil-rate bands

The freeze on IHT thresholds will be extended by an additional two years, to 2030. The nil-rate band and residence nil-rate band will remain at £325,000 and £175,000 respectively.

Pensions

Reeves announced she was closing the “loophole” that gives pensions preferable IHT treatment. She will bring unused pension funds and death benefits payable from a pension into a person’s estate for IHT purposes from 6 April 2027.

The government estimates this measure will affect around 8% of estates each year.

Agricultural Property Relief

Currently, individuals can claim up to 100% relief on agricultural property (land or pasture that is used to grow crops or rear animals).

From 6 April 2026, the first £1 million of combined business and agricultural assets will continue to attract no IHT at all. However, for assets above this threshold, IHT will apply with 50% relief.

Business Property Relief

From 6 April 2026, the government will also reduce the rate of Business Property Relief from 100% to 50% in all circumstances for shares designated as “not listed” on the markets of a recognised stock exchange, such as the AIM.

ISA subscription limits frozen until 2030

Prior to the Budget, there was speculation that the chancellor may make changes to simplify the ISA regime.

While these did not materialise, the Budget did confirm that annual subscription limits will remain at £20,000 for ISAs, £4,000 for Lifetime ISAs and £9,000 for Junior ISAs and Child Trust Funds until 5 April 2030.

Additionally, the starting rate for savings will be retained at £5,000 for 2025/26, allowing individuals with less than £17,570 in employment or pension income to receive up to £5,000 of savings income tax-free.

A change to business rates relief

The current business rates relief system is set to run until April 2025. It effectively serves as a reduction on business rate bills for eligible businesses, with retail and hospitality firms having been key beneficiaries.

The chancellor announced that, from 2026/27, permanently lower tax rates will be introduced for retail, hospitality and leisure properties.

Additionally, for 2025/26, some retail, hospitality, and leisure properties will receive 40% relief on their bills, up to a cash cap of £110,000 per business.

Corporation Tax capped at 25%

The government plans to support businesses to invest by publishing a Corporate Tax Roadmap. This confirms that the government will cap Corporation Tax at 25% for the duration of the parliament.

A rise in the national living wage

Reeves announced a 6.7% rise in the national living wage for workers aged 21 and over, from £11.44 to £12.21 an hour, effective April 2025. For a full-time employee earning the national minimum wage, this means a £1,400 annual pay boost and is expected to benefit more than 3 million workers.

In addition, the national minimum wage for people aged 18 to 20 will rise from £8.60 to £10 an hour. Apprentices will receive the biggest pay increase, with hourly pay rising from £6.40 to £7.55 an hour.

The announcement could significantly increase outgoings for businesses, particularly when coupled with reforms to employers’ NI.

A freeze in fuel duty

Fuel duty has been frozen since 2011, and the 5p cut brought in by the Conservatives in 2022 has been extended at every subsequent Budget.

Despite speculation that Reeves might increase fuel duty, she confirmed the freeze for another year and extended the 5p cut. This will save the average motorist £59 in 2025/26.

Second home Stamp Duty surcharge increasing

With effect from 31 October 2024, the Stamp Duty surcharge on the purchases of second homes, buy-to-let residential properties, and companies purchasing residential property in England and Northern Ireland will increase from 3% to 5%.

This surcharge is also paid by non-UK residents purchasing additional property.

Reforms to the non-dom regime

Currently, for UK residents whose main residence – or “domicile” – is elsewhere in the world, income and gains are taxed differently, depending on factors such as how long individuals are resident in the UK.

The chancellor confirmed that the tax regime for non-domiciled individuals (non-doms) will be abolished from April 2025, claiming that the rules will ensure that those who “make the UK their home will pay their taxes here”.

Moving forward, there will be a residence-based scheme with “internationally competitive arrangements” for those who come to the UK on a temporary basis.

Over the next five years, Office for Budget Responsibility (OBR) figures estimate that these reforms will raise £12.7 billion.

VAT on private school fees from January 2025

As they had promised in their election manifesto, Labour announced that, from 1 January 2025, VAT will apply to all education, training, and boarding services provided by private schools.

Additionally, the chancellor announced that she was removing business rates relief from private schools from April 2025.

An end to the £2 bus fare cap

The £2 cap on bus fares introduced by the previous Conservative administration is due to end on 31 December 2024.

Labour has announced that it will extend the cap for a further 12 months but that the cap will rise from £2 to £3.

Changes to duties for alcohol, tobacco, and vaping

The chancellor confirmed a reduction in the duty for draught alcohol, cutting duty on an average strength pint by a penny. Rates for non-draught products will increase in line with the Retail Prices Index (RPI) from 1 February 2025.

Furthermore, a new vaping duty will be introduced from 1 October 2026, standing at £2.20 per 10 ml of liquid. Meanwhile, there will be a one-off tobacco duty rise designed to maintain the incentive to choose refillable vaping over smoking.

Confirmation of the 4.1% increase to the State Pension under the triple lock

The basic and new State Pension will increase by 4.1% in 2025/26, in line with earnings growth, meaning over 12 million pensioners will receive up to £470 a year more.

Please note

All information is from the Autumn Budget documents on this page.

The content of this Autumn Budget summary is intended for general information purposes only. The content should not be relied upon in its entirety and shall not be deemed to be or constitute advice.

While we believe this interpretation to be correct, it cannot be guaranteed and we cannot accept any responsibility for any action taken or refrained from being taken as a result of the information contained within this summary. Please obtain professional advice before entering into or altering any new arrangement.

Investment market update: September 2024

Economic data suggesting some developed countries, including the US, could fall into a recession continued to affect investment markets in September 2024. Read on to discover other factors that may have affected the performance of your investments.

UK

Data from the Office for National Statistics (ONS) shows inflation remained stable at 2.2% in the 12 months to August. The figure is slightly above the Bank of England’s (BoE) 2% target.

Despite speculation that inflation data would lead to the BoE cutting interest rates, the Bank opted to maintain its base rate at 5%. While good news for savers, it means borrowers, including mortgage holders, are still likely to face higher outgoings when compared to 2021.

Many economists expect the BoE will make an interest rate cut before the end of the year. Indeed, investment bank Goldman Sachs predicts the interest rate will fall to 3% over the next 12 months.

GDP data showed the UK economy returned to growth in July after a plateau in June. However, the figures were disappointing, with just 0.5% growth in the three months to July 2024.

There could be more positive news in the coming months though. Investment bank Peel Hunt optimistically said the UK economy is heading for “above-average growth” as inflation stabilises and consumer demand picks up.

A report from the Office for Budget Responsibility (OBR) provided a less cheerful outlook for the UK. The latest risk and sustainability report warned the UK, and other countries in the world, face long-term pressures, such as an ageing population, climate change, and rising geopolitical tensions.

In addition, the OBR said, based on current policy, public debt is projected to almost triple to more than 270% of GDP over the next 50 years. The comments highlight the challenging backdrop chancellor Rachel Reeves will need to consider as she prepares to deliver her first Budget on 30 October.

There was positive data released from the manufacturing sector. S&P Global’s Purchasing Managers’ Index (PMI) recorded the strongest month in two years. Both output and new orders continued to recover.

Yet, many businesses continue to face significant headwinds. Among those is UK shipbuilder Harland & Wolff, which owns the Belfast shipyard that once built the Titanic. The company entered administration in September.

Research also suggests that trade difficulties following Brexit could worsen. Aston Business School analysed the effect of the Trade and Cooperation Agreement on UK-EU trade relations, and found that trade is down by almost a quarter.

The FTSE 100 experienced ups and downs, including falling 0.6% to a three-week low on 4 September. Susannah Streeter, head of money and markets at Hargreaves Lansdown, said: “Fresh worries about the health of the global economy have gripped markets, with the FTSE 100 far from immune.”

Europe

Eurozone inflation fell to 2.2% in the 12 months to August 2024. The news gave the European Central Bank the confidence to cut interest rates for the second time this year.

The Paris Olympics provided a short-term boost to the eurozone economy. A PMI output index increased for the first time since May in August 2024 to reach a three-month high of 51.0 – a reading above 50 indicates growth.

However, as the temporary boost of the Olympics fades, additional PMI data isn’t as positive. Indeed, HCOB’s flash PMI suggests the eurozone economy shrank for the first time in seven months in September.

The manufacturing sector in particular is struggling, with a PMI reading of 45.8 in August 2024. Dr Cyrus de la Rubia, chief economist at Hamburg Commercial Bank, said: “Things are going downhill, and fast. The manufacturing sector has been stuck in a rut.”

As the largest economy in the EU, the conditions in Germany can affect the bloc, and statistics suggest there are risks ahead.

Indeed, the Kiel Institute for the World Economy predicts Germany’s GDP will shrink by 0.1% this year and has halved its growth forecast for 2025 to 0.5%.

Statistics body Destatis reports industrial production in Germany fell by 2.4% in July – far more severe than the 0.3% fall economists had predicted. The automotive sector suffered the largest fall (8.1%) followed by electrical equipment (7%).

German carmaker Volkswagen has spoken about the challenges it faces. The company warned that it has a “year, maybe two” to adapt to lower demand. The economic environment has led to Volkswagen considering making unprecedented closures in its home market for the first time in its history as it tries to cut costs.

US

Inflation in the US fell to its lowest level since February 2021 in August 2024 to 2.5%. In response, the Federal Reserve cut its base interest rate from 5% to 4.75%.

The inflation and interest rate announcements led to the S&P 500 – an index of the 500 largest public companies in the US – jumping 1.5% on 19 September.

Similar to Europe, data indicates the manufacturing sector in the US is struggling. Indeed, the Institute of Supply Management reported it contracted for the fifth consecutive month in August. The news led to a dip in the markets around the world at the start of the month.

Figures from the Bureau of Economic Analysis also indicate a business threat as the trade deficit increased by $5.6 billion (£4.19 billion) in July to $103.1 billion (£77.13 billion).

American company OpenAI, the firm behind ChatGPT, announced it was in talks to raise $6.5 billion (£4.86 billion) from investors at a valuation of $150 billion (£112.21 billion) – making it one of the most valuable start-ups in the world.

Asia

Investment market volatility in Asia highlighted how factors around the world can affect markets. On 4 September, Japan’s Nikkei lost 4.2% and South Korea’s Kospi fell 3.4% after investors were spooked by fears that the US could experience a downturn when poor manufacturing data was posted.

A survey of China’s manufacturers from Caixin suggests export orders were subdued in August and fell for the first time this year as it faced external challenges.

However, China announced stimulus measures aimed at boosting the economy and stock market, as well as supporting the property sector on 24 September.

The news led to stock markets across Asia-Pacific rising – China’s CSI 300 index was up more than 4%. In fact, the announcement led to world stocks hitting a record high when the MSCI World Stocks index increased by 0.3%.

Please note:

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

Recent Comments