Category: News

Baffling financial jargon means Brits are overlooking ways to boost their wealth

Brits are struggling with financial jargon and aren’t sure where to start with investing. It could mean some people are missing out on opportunities to increase their wealth.

A survey from Lloyds Bank found that 50% of Brits say they were scared of investing. Furthermore, 38% say financial jargon is baffling.

Misunderstanding common financial terms could lead some people to make decisions that aren’t right for them.

Despite dominating the headlines over the last year, 3 in 10 people said they didn’t understand “inflation”. As inflation has a direct effect on your cost of living, not understanding how it influences your outgoings could mean some budgets are no longer realistic.

Other common investing terms people are clueless about include:

- Asset class (77%)

- Dividend (42%)

- Stocks (37%)

- Portfolio (37%)

- Shares (31%)

Uncertainty about financial terms mean that many people find learning about finances daunting. In fact, 26% of people believe it would be easier to learn a new language than start investing.

Yet, half of the participants said they wanted to learn more about the basics of investing and finances.

Overlooking investing could affect your long-term wealth

If a lack of financial confidence means you’ve not considered investing, you could be missing an opportunity to grow your long-term wealth.

While money in a savings account is “safe”, the interest it earns is likely to be below inflation, which reduces the value in real terms.

Inflation means the cost of goods and services is rising, so your money will gradually buy less. Unless the interest you earn on a cash account exceeds inflation, the spending power of your savings is falling in real terms.

As inflation is currently high, the value of your savings could be falling quickly. However, even when inflation isn’t high, the compounding effect may have a greater impact on your savings over the long term.

In some cases, investing could help grow your wealth. Historically, investment markets have delivered positive returns over the long term, which might provide a way to increase your wealth at a faster pace than inflation.

However, it is important to note that investing isn’t always the right option. For instance, if you’re saving for short-term goals, a cash account may be more appropriate. Or if you don’t have an emergency fund, focusing on building one first could provide you with greater financial resilience.

All investments carry some risk and returns cannot be guaranteed, so just as crucial as deciding whether to invest is choosing which investments suit you.

Here are three ways a financial planner could help improve your investment and financial knowledge.

1. Cut through confusing financial jargon

If you’ve been putting off financial decisions because jargon means you’re not sure which options are right for you, speaking to a financial planner could be useful.

We can not only explain what financial terms mean, but why they may be relevant to you. Having your options explained in clear language could give you the confidence to take control of your finances.

2. Assess which investments could be right for you

The survey suggests that many people don’t know where to start when they want to invest. It’s easy to see why – there are a lot of options to choose from, and it can be difficult to know which ones may be right for you.

To understand which investments suit your goals, you may need to consider areas like your investment time frame, what other assets you hold, and your risk profile. You should also keep in mind how different investments can be used to create a balanced and diversified portfolio.

A financial planner can assist with all of these, helping you build a financial plan to suit your needs and circumstances.

3. Provide you with someone to turn to when you’re uncertain

Even the best-laid plans can go awry. Perhaps, health reasons mean you want to stop working sooner than expected. Or investment market volatility means the value of your portfolio has unexpectedly fallen.

Working with a financial planner on an ongoing basis means you have someone to turn to if you need reassurance or would like to update your financial plan. They can also help ensure your financial decisions continue to reflect your goals and economic circumstances.

Contact us to talk about your finances

If you want help creating a financial plan that suits you, please get in touch. We can offer advice and guidance so you can feel more confident taking control of your long-term finances.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

The value of your investment can go down as well as up and you may not get back the full amount you invested.

Past performance is not a reliable indicator of future performance.

A grocery shop would cost just 45p in 1940s when the first supermarket opened its doors

Visiting the supermarket to pick up a few items or do your weekly shopping is so common it can be difficult to imagine life without this convenience. Yet, it wasn’t too long ago that the first supermarket was opening its doors in the UK. And looking back offers an interesting insight into how money and shopping habits have changed.

The London Co-operative Society opened its doors for the first time in 1948.

It offered a very different service to other shops of the time. Shoppers were used to chatting with the shopkeeper while an assistant picked the items for them. In fact, shoppers wouldn’t have handled the goods at all until they paid.

So, walking into a “self-service” supermarket – where customers picked up their items themselves and took them to a till – was a very different experience. On top of that, there were all kinds of goods under one roof and competitive prices. It’s easy to see why supermarkets became popular.

Today, there are thousands of supermarkets across the UK, from the “big six” to independent stores. And “self-service” has gone one step further with many shops installing checkouts customers can use themselves.

In the 75 years since the first supermarket opened, how we use money, the value of it, and shopping habits have changed enormously. Looking at inflation and how it’s calculated offers a glimpse into this transition.

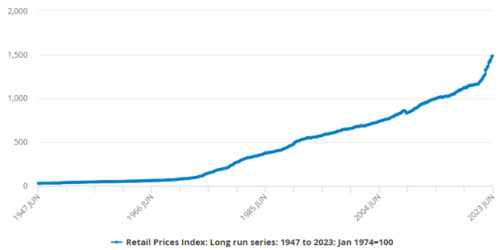

£1,000 in 1946 has the same value as almost £34,500 today

The UK first started tracking retail prices a year after the first supermarket opened. It shows how prices have changed over seven decades.

Data from the Office for National Statistics (ONS) demonstrates how inflation influenced prices between 1947 and 2023. While there have been times retail prices have dipped, overall, it’s been an upwards trend.

Source: Office for National Statistics

In fact, according to the Bank of England’s inflation calculator, £1,000 in 1946 would be equivalent to almost £34,500 today.

The ONS measures inflation by tracking a “basket of goods”. This basket is filled with common goods and services to understand how the cost of frequent purchases changes. Currently, there are around 700 representative consumer goods and services in the basket. As well as groceries from the supermarket, it also includes items like clothing and electronics.

The items are regularly reviewed. So, not only does it track prices, but trends and spending habits.

When the first supermarket opened, rationing was still in place. In the post-war era, the ONS included items like condensed milk, which was often used to make rations stretch further. Condensed milk remained in the basket until 1987 when fresh, pasteurised milk became more widely available.

Fast forward to 2023, and new additions to the basket include frozen berries and free-from products.

3 interesting comparisons that show the power of inflation

1. The average salary was 126 shillings, 9 pence

Before the government introduced decimalisation in 1971, there were 20 shillings to a pound and 12 pence to a shilling. According to the House of Commons library, the average worker earned 126 shillings, 9 pence a week in November 1946.

Inflation means the average earnings in April 2023 are significantly more. Data from ONS shows the average weekly salary is £603, excluding bonuses.

2. A weekly grocery shop was just 45p

According to the Northumberland Gazette, the average person needed just 45p to pick up a week’s worth of groceries in the 1940s. In today’s money that would be less than £20.

However, food inflation and changing habits mean the average adult spends around £44 a week on food in 2023.

3. A property “boom” led to prices quadrupling in some areas

Soaring property prices are often discussed in newspapers today, and it’s not a new phenomenon.

A 1947 article in the Guardian states there was a “boom in house property prices”. In 1939, houses went for around £500. Just eight years later, aspiring homeowners could expect to pay up to £1,500, or even up to £4,000 in select residential districts.

Over the next seven decades, house prices outstripped inflation. The Halifax House Price Index suggests the price of an average house in June 2023 was more than £285,000.

Have you considered how inflation could affect your finances?

Since the first supermarket opened its doors, inflation has affected the value of money. This is something you may need to consider when managing your finances.

For example, if you’re planning for retirement in 20 years, how will the income you need to maintain your lifestyle change? How can you grow your assets to keep up with the pace of inflation?

A financial plan that incorporates inflation could help you understand how it may affect your wealth and the steps you might take to protect it. Please contact us to arrange a meeting to discuss your financial plan.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

Investing 101: What you need to know about tax efficiency and your investment options

Investing may provide a useful way to grow your wealth, but getting started can be overwhelming. There are some important decisions to make when investing that could affect the outcomes and the tax you’re liable for, and we’re here to offer support.

Last month, you read about investment risk and what to consider when creating a risk profile. Now, read on to discover what your options are if you’re ready to start investing.

Shares v funds: What’s the difference?

Investing is filled with terms that can seem confusing. When you’ve looked at investing, you may have come across options like investing in shares or through a fund.

You may want to consider both options and understanding the differences is important.

Shares

When you purchase a share, you’re investing in a single company. When you hold a share, you essentially own a very small portion of the business. You can then sell the share at a later date and, hopefully, make a profit.

The value of shares is affected by demand. A whole range of factors can affect demand, from company performance and long-term plans to global economic conditions.

If you purchase shares, you’re in control and can decide which companies to invest in and when to sell them.

It’s normal for the value of shares to fluctuate, even daily. It can be tempting to try and time the market by buying when the price of a share is low and selling when it’s high. However, consistently timing the market is impossible. For most investors, buying shares to hold them for the long term often makes sense.

Funds

A fund pools together your money with that of other investors. This money is then used to purchase shares in a range of companies.

A fund is managed on behalf of investors. So, you wouldn’t make decisions about which companies to invest in or when to buy or sell shares.

There are lots of funds to choose from, so you can select an option that suits your risk profile and goals.

Funds can be a useful way to ensure your investments are diversified. As your money is spread across many companies, it can help create balance. When one company performs poorly, the success of another could balance this out. So, the value of your investment in a fund may be less volatile than individual shares.

However, the value of your investment will still rise and fall, and investing with a long-term plan is often advisable.

2 tax-efficient ways to invest and reduce your potential tax bill

When you sell certain assets and make a profit, you could be liable for Capital Gains Tax (CGT). This includes investments that aren’t held in a tax-efficient wrapper.

For the 2023/24 tax year, individuals can make £6,000 of gains before CGT is due – this is known as the “annual exempt amount”. If profits from the sale of all liable assets exceed this threshold, you could face a CGT bill. In 2024/25, the annual exempt amount will fall to £3,000.

The rate of CGT depends on your other income, but when selling investments, it can be as high as 20%. So, CGT may significantly affect your profits.

The good news is that there are tax-efficient ways to invest that could reduce your bill, including these two:

1. Invest through a Stocks and Shares ISA

ISAs provide a tax-efficient way to save and invest. For the 2023/24 tax year, you can add up to £20,000 to ISAs. The returns made on investments held in a Stocks and Shares ISA are not liable for CGT.

There are many ISAs to choose from. They can hold shares or you can invest in a fund through one. Usually, you can access your investments that are held in an ISA when you choose.

2. Use your pension to invest for the long term

If you’re investing with your long-term wealth in mind, you may want to consider pensions. Pensions are tax-efficient for two reasons.

- First, you could claim tax relief on the contributions you make. This provides a boost to your contributions, which may grow further too, as tax relief would be invested alongside other deposits.

- Second, your investment returns are not liable for CGT when held in a pension. Instead, you could pay Income Tax when you start to access your pension once you reach retirement age.

In 2023/24, you can usually add up to £60,000 (up to 100% of your annual earnings) into a pension while retaining tax relief – this is known as your “Annual Allowance”.

If you are a high earner or have taken an income from your pension already, your Annual Allowance may be lower. Please contact us if you’re not sure how much you can tax-efficiently save into a pension.

Before you start investing in a pension, one key thing to consider is when you’ll want to access the money. Usually, you cannot make withdrawals from your pension until you are 55, rising to 57 in 2028. So, your goals and other assets should play a role in deciding if investing more into a pension is right for you.

Contact us if you have questions about your investment portfolio

We can work with you to create an investment portfolio that suits your risk profile and goals. We’re also on hand to answer any questions you may have, from deciphering financial jargon to explaining tax-efficient options. Please contact us to arrange a meeting to talk about your investments.

Once you’ve set up an investment portfolio, how often should you review the performance? Why is ongoing advice useful? Read our blog next month to learn about managing investments on an ongoing basis.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Investment market update: March 2023

As inflation persists, central banks were forced to announce further rises to interest rates in March.

Coupled with the collapse of Silicon Valley Bank, it has been an uncertain few weeks in the world economy.

As an investor, remember that volatility in the markets is normal. Take a long-term view of your portfolio’s performance and focus on your overall goals rather than short-term market movements.

Here are some of the factors that affected markets in March 2023.

UK

After hitting a new record high in February 2023, the FTSE 100 fell back in March. Indeed, in mid-March, the index suffered its worst day of trading since the start of the Covid-19 pandemic.

Overshadowing the spring Budget and sparked by fears over the health of the global banking sector, the FTSE 100 closed 292.66 points lower – around 3.8% – on 15 March.

In a Budget the chancellor called “a plan for growth”, the key announcements included:

- An extension of the Energy Price Guarantee scheme until the end of June 2023

- The removal of the pensions Lifetime Allowance (LTA) tax charge from 2023/24, with plans to abolish the LTA in a future Finance Bill

- A year-long extension to the 5p cut to fuel duty on petrol and diesel, due to end in April

- Rises in various pension allowances to encourage more tax-efficient retirement saving

- Plans to create a dozen new investment zones that could become “12 potential Canary Wharfs”

- A policy of “full capital expensing”, initially for the next three years, which will allow firms to write off all investment against their tax bills.

While the UK remains the only country among the G7 major economies that has yet to fully recover its lost output during the Covid-19 pandemic, it is defying predictions of a recession.

The UK economy grew by 0.3% in January with the largest contributions to growth coming from education, transport and storage, and arts, entertainment and recreation activities, all of which have rebounded after falls in December 2022.

Inflation unexpectedly rose in the year to February 2022, with the Office for National Statistics reporting that rises in restaurant and cafe, food, and clothing costs pushed the annual rate up to 10.4%.

This led to the Bank of England increasing the base interest rate for the 11th consecutive time, to 4.25%.

Europe

Recession fears continue in the eurozone, with GDP growth revised down to 0.0% in the fourth quarter. Household consumption in the fourth quarter of 2022 saw the largest decline since the start of the eurozone in 1999, with the exception of during the Covid-19 pandemic.

Headline inflation in the eurozone remains high – it stood at 8.5% in February – and this led the European Central Bank (ECB) to increase interest rates by 0.5 percentage points in March. This pushes the bank’s main rate up to 3.5%, while the rate paid on eurozone bank deposits left at the ECB increases to 3%.

Christine Lagarde, the president of the ECB, said the central bank would treat the heightened tensions in financial markets separately from its strategy for bringing down inflation.

As with the leading UK and US indices, the STOXX 600 index fell in the aftermath of the SVB crisis, and has remained uncertain due to ongoing economic concerns.

US

The economic headlines in the US in March were dominated by the collapse of Silicon Valley Bank (SVB) – the country’s 16th largest bank.

Since the pandemic began, SVB had been buying lots of what are often considered “safe” assets such as US Treasury bonds and government-backed mortgage bonds. When interest rates started to rise sharply, their fixed interest payments didn’t keep up with rising rates.

Those assets were then no longer worth what SVB paid for them, and the bank was sitting on more than $17 billion in potential losses on those assets as of the end of last year.

In early March, SVB then faced a wave of $42 billion of deposit withdrawal requests. As it wasn’t able to raise the cash it needed to cover the outflows, regulators were forced to step in and close the bank.

While both the US and UK governments ensured that customers of the stricken bank were protected, it has raised fears of another global banking crisis. Indeed, Credit Suisse, one of the world’s oldest banks, was bought by rival UBS in a Swiss government-backed deal in March after regulators worked frantically to secure a deal for the loss-making bank.

Fears of another banking crisis have led to volatility in US markets, with some economists modestly lowering their forecasts for economic growth this year because of the SVB crisis as smaller banks restrict lending in an already weak environment.

Inflation in the US fell to 6% in February 2023, down from an annual rate of 6.4% in January and significantly lower than the 9.1% peak of inflation seen in June 2022.

Despite the uncertainty in the markets, the Fed raised interest rates by 0.25 percentage points in March, taking the upper limit of US interest rates to 5%, the highest level since 2007.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Financial planning as a couple could boost your finances, but almost 2 in 5 admit to “financial infidelity”

Research has found that many couples keep financial secrets. While you may want to keep your finances separate for a whole host of reasons, working together could mean your money goes further and you’re more likely to reach your goals.

According to an Aviva survey, 38% of people in a relationship admit to having a secret account or money stashed away that their partner doesn’t know about. The average amount hidden in a savings account is £1,600, and half of over-55s have more than £2,000 squirrelled away.

There are lots of motives for keeping some money to yourself. 32% of people said it was because they wanted to maintain control of their finances. A quarter said it was so they could treat themselves without their partner knowing, while a similar proportion are doing so to create a nest egg for their child.

As well as savings accounts, it’s not uncommon for couples to keep other financial secrets.

Perhaps you haven’t told your partner how much you have saved in your pension, or how well your investments have performed?

Whatever your reasons for keeping some of your finances to yourself, it’s worth considering if creating a financial plan together could be useful.

3 fantastic reasons to plan as a couple

Creating a financial plan with your partner can be incredibly useful and mean you both have more confidence about the future. If you’re not already planning with your partner, here are three fantastic reasons you should think about it.

1. It provides an opportunity to talk about your attitude to money

Money can be a difficult subject to discuss. If you have different views about money from your partner, it can lead to arguments.

The Aviva survey found that 26% of people said they bicker about money at least once a week. Unsurprisingly, the cost of living crisis is putting more pressure on couples, and 34% said they are arguing about money more.

A financial plan can facilitate an open conversation about your attitude to money and how you use it. It’s a process that can help you better understand your partner’s point of view and ease tensions.

2. Benefit from a clear goal that you’re both working towards

Financial planning isn’t just about maximising your wealth – in fact, far from it. The key benefit of financial planning is that it creates a plan that’s designed to help you reach your goals.

So, planning as a couple can mean you’re both working towards the same future. Whether you hope to retire early or are keen to give your children a financial head start when they reach adulthood, a financial plan will be tailored to suit your goals.

Setting this out as a couple can mean you’re both on the same page and motivated to take the steps necessary to secure the future you want.

3. Make the most of tax allowances

As a couple, there may be tax allowances you can take advantage of by planning as a couple.

For example, the Marriage Allowance could lower your combined Income Tax bill if one of you doesn’t earn more than the Personal Allowance, which is £12,570 for the 2023/24 tax year.

Splitting assets between you could also mean you can make the most of tax breaks. Each individual can add up to £20,000 each tax year to an ISA to save or invest tax-efficiently. So, spreading cash between both of your ISAs could reduce your overall tax bill.

Similarly, for the 2023/24 tax year, you can make up to £6,000 profit when disposing of some assets, including investments that aren’t held in a tax-efficient wrapper, before Capital Gains Tax (CGT) is due. As you can pass on assets to your spouse or civil partner without having to pay CGT, doing so could mean you could make profits of up to £12,000 before becoming liable for tax.

Contact us to arrange a meeting with your partner to create a financial plan

Working together towards common goals doesn’t have to mean merging all of your assets. You may choose to keep some, or even all, assets separate. There’s no one-size-fits-all solution when creating a financial plan – it’s about what works for you and your partner.

Please contact us to arrange a meeting to discuss your finances and aspirations for the future. We can help you implement a plan that you feel comfortable with.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

This article is for information only. Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

What does the multiverse theory have to do with cashflow modelling? Find out here

Financial planning doesn’t have a lot in common with science fiction. Yet, cashflow modelling could allow you to explore the lives you could lead if you made different decisions. So, it has more in common with the multiverse theory than you might initially think.

The multiverse theory suggests there is a hypothetical group of multiple universes with many different worlds. It proposes that every time an outcome is observed, there is another “world” in which a different outcome becomes reality.

So, while here you may have made certain career decisions, or started a family, there are countless other realities where you’ve made different choices.

Despite some scientists searching for evidence to support the multiverse theory, they haven’t found any yet, and others are sceptical. Yet, it’s continued to be a huge source of inspiration in science fiction.

Indeed, one of this year’s Oscar nominations Everything Everywhere All at Once suggests that every decision you make creates a parallel universe. You can see the influence of the theory in literature too, from Matt Haig’s Midnight Library to thriller Recursion by Blake Crouch.

But, what does the multiverse theory have to do with cashflow modelling?

You can “test” your decisions through cashflow modelling

Cashflow modelling can forecast your future finances in different scenarios.

You start by inputting information, such as how much you have in savings, the value of your investments, or your income. By making certain assumptions, like expected investment returns or income growth, you can project how your wealth will change over your lifetime.

Once the information has been added to a cashflow model, you can then model different scenarios and take a peek into what could happen in those other realities. You can see how decisions you make, or things outside of your control will affect your financial future.

Let’s focus on investments. A cashflow model could show what may happen if:

- You increased how much you invested by 10% each month

- Investment returns were 5% or 7% a year

- You used your investment portfolio to boost your retirement income by £5,000 a year.

Sadly, cashflow modelling doesn’t let you experience other lives like you see in films. But it can help you visualise different scenarios and how the decisions you make could lead to very different outcomes.

2 compelling reasons to make cashflow modelling part of your financial plan

1. It can give you confidence in your financial decisions

As cashflow modelling can help you understand how your decisions could affect your wealth in the short, medium, and long term, it can give you confidence.

If you’ve been deliberating over whether you can afford to give your child a property deposit, or if you have enough to retire early, cashflow modelling could mean you’re able to move ahead with plans with fewer doubts. By understanding the implications of your financial decisions, you can focus on what’s important in your life.

2. It can help you prepare for different outcomes

One of the challenges of creating a long-term financial plan is that things outside of your control can affect it. Cashflow modelling can help you answer “what if?” questions like:

- What if I was forced to retire earlier than expected due to ill health?

- What if my investments don’t perform as well as hoped?

- What if I passed away? Would my spouse and children be financially secure?

By modelling these types of scenarios, you can see what effect they would have on your wealth and lifestyle. That puts you in a position to prepare for them to give you peace of mind. It could include putting more away for your retirement now or taking out life insurance to provide for your family if you pass away.

As a result, cashflow modelling can mean you and your loved ones are more financially secure and better prepared to overcome unexpected life events.

Are you ready to consider the multiverse? Get in touch

If you want to better understand how the financial decisions you’re making could affect your life in the future, please contact us. We can help you visualise different outcomes, and then create a financial plan that could turn your aspirations into reality.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

51% of adults don’t have a will. Here’s why it should be a priority task

The benefits of having a will in place are well-documented, although if you don’t have a will, or haven’t updated it in some time, you’re not alone. A recent survey from MoneyAge has found that 51% of adults in the UK currently don’t have a will in place.

Of those with a will, 43% haven’t updated it since it was first written.

A will can be a fantastic way to:

- Allocate your assets to loved ones

- Nominate legal guardians for your children

- Divide your estate as painlessly as possible

- Reduce your liability for Inheritance Tax.

If you don’t have an up-to-date will, there’s a chance your loved ones won’t receive the wealth you intended for them. So, continue reading to discover why having an up-to-date will is vital.

It ensures your assets pass to the people you want them to

Perhaps the most obvious benefit of having an up-to-date will in place is knowing your assets will pass to the people you wish.

If you die without a will in place, or “intestate”, you’ll have no say over how your assets will be distributed. Instead, the laws of intestacy will dictate how your estate is divided.

This is especially important if you have a partner and you’re not married. While your blood relatives and/or spouse will usually inherit according to the laws of intestacy, a cohabiting partner and any stepchildren you have will likely not.

Your will is the perfect way to dictate where you want your money to go after you pass away, giving your loved ones more financial security after you die.

It could mean less hassle for your family

After you die, your family will need to administer your estate. This can be a stressful process, especially while they’re dealing with the grief of your passing. So, having a will in place that clearly outlines your wishes may make it easier for your family to make any necessary arrangements.

For instance, if you don’t have a will, dividing your estate could be incredibly stressful and time-consuming, and it could take longer for your assets to pass to your loved ones.

It could help avoid disputes

As mentioned, it’s a common occurrence for families to experience periods of heightened stress and grief after you die. As such, the dividing of an estate can be the perfect storm of stress and emotion, which can, unfortunately, often lead to disputes.

Indeed, data from IBB Law shows that 75% of people are likely to experience a will or inheritance dispute case at some point in their life.

Disputes can have lasting adverse effects on your family – they could permanently damage relationships or even cause schisms in the family, not to mention costing thousands in legal fees.

With a will in place, these disputes could potentially be avoided, making the process of dividing your estate as simple and painless as possible.

Even if you already have a will, you’ll need to update it regularly as your circumstances change. For example, if you remarry your existing will is automatically revoked. So, if you don’t write a new one, your estate could pass to the “wrong” people and cause arguments or disputes.

You can assign guardians for your children

While you may think your will is only used to allocate your estate, it can also be used to express your wishes about what will happen to your children after you die.

If your dependents are below the age of 18, you can use your will to nominate legal guardians. If you don’t nominate a guardian in your will, a family court would need to decide what happens to your children and their care could be left in the hands of a person you wouldn’t have chosen.

Even if you do have a will, it may be worth updating it regularly to fit your current circumstances – for example, as you have more children.

You could potentially mitigate an Inheritance Tax bill

When you die, the total value of your estate will dictate the amount of Inheritance Tax (IHT) that will be payable.

As of the 2023/24 tax year, the IHT threshold stands at £325,000, though you can also benefit from the additional £175,000 “residence nil-rate band” if you leave your home to a direct descendant, such as a child or grandchild.

Then, anything left in your estate above this threshold will typically be subject to the standard IHT rate of 40%.

With a well-written will, you can often reduce your IHT liability. For example, suppose you specify that you want your home left to a direct lineal descendant. In this case, you could make full use of the additional residence nil-rate band, substantially reducing the IHT liability of your estate.

Wills can help you to make your estate plan as tax-efficient as possible.

It ensures that nothing is left behind

After you die, there will be plenty of paperwork relating to your finances that your family will need to deal with.

If you haven’t clearly outlined your assets in your will, your family could miss something they didn’t know existed, such as a previous pension, an old savings account, or even any protection you had.

When your will is in place, you can clearly identify your assets and distribute them to your beneficiaries. This could ensure that your family doesn’t miss out on any of your hard-earned wealth.

This is another great reason to update your will regularly. If you have acquired assets later in life and fail to update your will to include them, they could be missed out entirely when your estate is divided.

It can give you peace of mind

Another beneficial reason to have a will in place is that it gives you the peace of mind that your affairs will be dealt with in the way you desire after you die. You can rest assured that your loved ones’ future is secure, and you can start living in the present.

For instance, if you die without a will, the intestacy laws will rule on issues ranging from the guardianship of your children to the dividing of your estate. If you write a will now, you can regain control and relax, knowing that the right people will receive your assets after you die.

Please note:

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

The Financial Conduct Authority does not regulate estate planning, tax planning or will writing.

4 valuable ways a financial planner can help you tackle “overwhelming” pension information

Do you find pension information confusing? You’re not alone; 50% of people in the UK describe the information they receive about their pension as “overwhelming”, according to a Standard Life study.

Fortunately, there are places where you can seek guidance or advice. The survey found 83% of people think financial advisers offer useful support.

If you’re not sure if your pension is on the right track, a financial planner could help put your mind at ease. Here are four reasons why.

1. A financial planner can cut through jargon

Pension information can be filled with jargon that makes it difficult to understand exactly what it is saying.

From “annuities” to the “Tapered Annual Allowance”, a financial planner could help you cut through confusing terms and take the time to explain what they mean and, more importantly, whether they’re relevant to you.

Having someone you can turn to for answers that you know you can rely on is invaluable.

2. A financial planner can help you make sense of pension statements

Your pension provider will provide a statement each year; this may come in the post or be online.

It will cover pension contributions, including your own, those made by your employer, and tax relief. These figures can help you understand how much is going into your pension.

As your pension will usually be invested, the statement is likely to include investment performance too. As investments can be volatile, it can be difficult to know whether your investments are performing well or not, and it’s also essential to ensure they match your risk profile and goals. As financial planners, we can help you get to grips with pension investments.

In addition, your pension statement will include a forecast. This is a projection based on assumptions that the provider makes, including your retirement date and investment performance, so it’s not a guarantee.

The pension forecast can be incredibly useful when thinking about how your savings will add up to deliver a retirement income. But understanding if it’s “enough” is another challenge.

3. A financial planner can help you calculate if you’re saving “enough”

Calculating how much you should be saving into your pension can be complex. There’s no one-size-fits-all figure, so you’ll need to consider your circumstances and goals to understand what is “enough”.

Not only will you need to calculate potential investment returns, but also the income you need to create the retirement lifestyle you want. As a result, setting a pension target often means pulling together different pieces of information, from life expectancy to other assets you’ll use to create an income, like savings.

A financial plan can help you understand what is “enough” for you to retire on, and, importantly, the steps you can take to reach the goal. With a clear blueprint, you’re more likely to retire with enough savings to live the lifestyle you want.

4. A financial planner can create a plan that means you can enjoy retirement

A financial plan can help you get the most out of your money, and allow you to really enjoy your retirement.

There’s strong evidence that taking control of your finances could boost your wellbeing. In fact, 93% of people that planned for retirement with an income of less than £20,000 say they are enjoying life after giving up work. However, only 66% of people that didn’t plan could say the same.

Despite this, 7 in 10 people are doing very little, if anything, to plan for their retirement.

So, arranging a meeting now to create a plan for when you give up work means you’re more likely to enjoy the next stage of your life. It’s never too soon to start retirement planning, and doing so earlier could grant you more freedom in the future.

Contact us to talk about your pension

If you want to talk about your pension and start thinking about what it means for your retirement, please contact us. We’ll work with you so you can have confidence in your retirement savings and look forward to the milestone.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future results.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates and tax legislation may change in subsequent Finance Acts.

Estate planning: Do you need to include Inheritance Tax?

Inheritance Tax (IHT) can affect what you leave behind for loved ones. It’s essential you understand if it’s something you need to think about, as there could be steps you can take to reduce a potential bill.

Over the last few months, you’ve read about what estate planning is and how to calculate the value of your estate. Mitigating an IHT bill should be an important part of your estate plan if you could be liable for it. Read on to find out when IHT is due.

The standard rate of Inheritance Tax is 40%

With a standard rate of 40%, IHT could substantially reduce the value of what you leave behind for loved ones. According to HMRC, around 3.76% of estates pay IHT.

IHT is a tax on your estate after you pass away if the total value exceeds certain thresholds. There are two allowances that you could use:

- If the value of your estate is below the nil-rate band, your estate will not be liable for IHT. For the 2023/24 tax year, it is £325,000.

- Should you leave your main home to your children or grandchildren, you may also be able to use the residence nil-rate band. For the 2023/24 tax year, it is £175,000.

As a result, you could leave up to £500,000 before IHT is due.

You can also pass on unused allowances to your spouse or civil partner. So, if you plan as a couple, you could leave an estate valued at up to £1 million before it’s liable for IHT.

The portion of your estate that exceeds these allowances is usually taxed at 40%.

Let’s say you leave behind assets worth £600,000 to your child, including your main home to take advantage of the residence nil-rate band. The first £500,000 can be passed on without being liable for tax. However, there would be a tax charge of £40,000 on the £100,000 that exceeds the allowances.

You should note both the nil-rate and the residence nil-rate band are frozen at the current level until April 2028. While the value of your estate is below the threshold now, will this still be the case in five years?

To plan effectively, you should consider how the value of your estate could change.

A plan is essential if you want to mitigate Inheritance Tax

There are often steps you can take to reduce a potential IHT bill. Creating a plan now could mean your loved ones inherit more of your estate.

There are lots of steps you can take to reduce IHT during your lifetime, including:

- Gift assets during your lifetime. You could support your loved ones by gifting assets now or during your lifetime. However, keep in mind that only some gifts will be outside of your estate for IHT purposes immediately. Others may still be included when calculating IHT for up to seven years. Contact us to discuss how to gift to reduce IHT liability now.

- Place assets in a trust. Placing assets in a trust could mean they are outside of your estate and, in some cases, you may still be able to benefit from the assets. You will need to name a trustee that will manage the assets on behalf of your beneficiaries. Trusts can be complex, especially if you need to consider IHT, so professional advice can be useful.

- Leave some of your assets to charity. This could bring the value of your estate below the IHT threshold. If you leave more than 10% of your entire estate to charity the IHT rate will fall from 40% to 36%, which could lower the bill for some families.

- Keep the value of your estate below the IHT threshold by spending. Make the most of your later years by spending more – it could mitigate an IHT bill if it brings the value of your estate below the threshold for paying IHT.

There may be other things you can do too. Contact us to create a tailored estate and IHT plan.

As well as steps to mitigate IHT, you may also want to create a plan for paying a bill. This could include setting money aside so it’s there when your family need it.

Another option is to take out a life insurance policy. You’d need to pay premiums and the policy proceeds could give your family the cash they need to cover an IHT bill.

You must ensure a life insurance policy that’s intended to cover IHT is written in trust, otherwise, the payout will be considered part of your estate when calculating IHT.

Contact us to talk about your estate plan and Inheritance Tax

If you’d like help understanding if your estate could be liable for IHT, or you want to discuss your options to potentially reduce a bill, please get in touch.

While estate planning often focuses on organising your affairs to pass on assets when you die, it can also cover steps to improve your long-term financial security. Next month, read our blog to discover what steps you could take to make your later years more secure.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

The Financial Conduct Authority does not regulate estate or tax planning.

Investment market update: December 2022

2022 ended with uncertainty and volatility that’s persisted for much of the year. Read on to find out what happened in December and how it affected investment markets.

Looking ahead, uncertainty is likely to be something investors will need to negotiate in 2023 too. As economies continue to struggle with high levels of inflation, Goldman Sachs CEO David Solomon warned that “bumpy times” were still ahead.

Keep in mind that volatility is part of investing and you should keep your long-term plan in mind when reviewing performance. You should also consider your risk profile and the investment opportunities that are appropriate for you.

UK

Inflation fell slightly in the 12 months to November 2022 to 10.7%. It’s led to hopes that inflation has peaked, but high levels are expected to persist in the first half of 2023. In response to inflation, the Bank of England (BoE) increased interest rates again, this time by 0.5% to 3.5%.

The soaring cost of living has led to strikes across the country, which has affected a range of services, from post to transport. Dubbed the “winter of discontent” by the media, figures from the Office for National Statistics (ONS) show that strike action is at its highest level for more than a decade. Around 417,000 working days were lost due to labour disputes in October.

One positive piece of data released in December was the GDP figure. It’s estimated that GDP grew by 0.5% in October after falling 0.6% in September.

However, experts have warned that the economy is still likely to fall into a recession. The Institute of Directors explained that the latest figure was most likely due to the extra bank holiday in September for the Queen’s state funeral, rather than the economy bouncing back.

Readings from S&P Global’s purchasing managers index (PMI) suggests that business output is falling. A reading below 50 indicates contraction.

- A “lethal cocktail” of Brexit, logistic challenges, high costs, and falling demand, means that the PMI for UK factories fell to its lowest level since April 2020, when the first wave of Covid-19 affected operations. The 46.5 reading suggests business is contracting.

- The reading for the service sector fell to 48.8 as cost of living challenges hit discretionary spending.

- The construction sector is still growing, although it is near the 50 mark, which indicates stagnation due to the rising cost of borrowing affecting the industry.

Businesses are also struggling to find the talent they need. According to an ONS survey, a third of UK businesses with 10 or more employees said they are experiencing a shortage of workers. This rises to 54% in the human health and social work sector.

While many businesses are suffering from falling demand, one bright spot was car sales. They increased for the fourth consecutive month. Industry leaders said a recovery for the sector was “within grasp” after November sales were 23.5% higher when compared to a year earlier.

US carmaker Ford also unveiled investment plans. It will invest an extra £125 million in its Merseyside factory to make electric vehicle parts. The move is part of the company’s zero-emission goals.

Europe

In a similar move to the BoE, the European Central Bank increased its base interest rate by 50 basis points due to inflation.

PMI data suggests that the eurozone is falling into a recession. Private sector output fell as demand for goods and services contracted. Job creation was also at its weakest level in almost two years as businesses are affected by uncertainty.

While manufacturing increased slightly when compared to the previous month. The PMI figures show it’s still in contraction as new orders fall.

This falling demand is affecting Germany, which is the largest economy in the eurozone. Exports declined by 0.6%.

USA

Statistics from the US paint a mixed picture. Like other economies, the US is facing high inflation, rising interest rates, and uncertainty.

PMI data suggests industries are contracting. For instance, the reading for the service sector fell from 47.8 in October to 46.2 in November.

However, job data suggests that businesses are still optimistic. The job market was positive, with 260,000 new jobs added in November. The unemployment rate also remained at 3.7% – an almost 50-year low. The figures indicate that businesses feel confident enough to invest in their workforce.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Recent Comments