Month: April 2024

Investment market update: March 2024

While inflation continues to be a challenge for many economies, there are positive signs in the UK and around the world. Read on to find out what may have affected stock markets and your investment portfolio in March 2024.

Remember, volatility is part of investing and most people should invest with a long-term outlook. If you have any questions about your investment strategy or performance, please contact us.

UK

In March, chancellor Jeremy Hunt delivered the 2024 Budget and set out the government’s spending and changes to taxation. One of the big announcements was a 2% cut to employee National Insurance, which follows a previous cut made in the 2023 Autumn Statement.

The Resolution Foundation, a thinktank, said pensioners were among the biggest losers in the Budget, as National Insurance is paid by workers but not people who are retired.

Investment bank Citigroup responded to the Budget by saying the Office for Budget Responsibility (OBR) was being too optimistic when it assumed productivity would grow by 0.9%. The organisation predicts a more modest 0.5% and said it means the UK could be “fiscally offside by around £50 – £60 billion”.

The OBR recognised that productivity has been poor since the 2008 financial crisis. In fact, growth has fallen from 2.5% a year to 0.5% – the economy would have been around 30% bigger today if the pre-2008 trend had continued.

David Miles, a member of the OBR, said the last 15 years have been so bad, that the next 5 to 10 years are likely to be a “bit better”. He particularly noted that AI could help boost productivity.

Inflation continued to fall in the 12 months to February 2024, with a rate of 3.4% – the lowest since September 2021.

Despite the positive news, the Bank of England (BoE) held its base interest rate at 5.25%. Huw Pill, chief economist at the BoE, said he believed more compelling evidence was needed before a cut would be made and it could be “some way off”.

The UK fell into a technical recession at the end of 2023, but the BoE said signs suggest it is already over.

Figures from the S&P Global Purchasing Managers’ Index (PMI) also support this. Private sector growth hit a nine-month high in February, indicating that the recession was shallow. However, the manufacturing sector continued to face challenges, with PMI data showing weak demand and supply chain disruption are contributing to a downturn.

Despite figures from the Insolvency Service indicating businesses are struggling, as insolvencies hit a 30-year high in 2023, there is some good news for investors.

The FTSE 100 – an index of the 100 largest companies listed on the London Stock Exchange – hit a 10-month high on 21 March when it increased by around 1.1%. Mining stocks were among the main risers amid expectations that the US Federal Reserve will cut its base interest rate soon.

Greggs also saw its stock rise during March. The bakery chain revealed like-for-like sales increased by 13.7% in 2023, while pre-tax profits jumped 27% to £188.3 million. The firm added it expected another year of good progress in 2024.

Europe

According to data from Eurostat, inflation across the eurozone continued to fall in February 2024, when it was 2.6% compared to 2.8% a month earlier.

While many countries in Europe are battling high inflation, Turkey’s rate of inflation has consistently been in double digits since the end of 2019. In February, it hit a 15-month high of 67%. In a bid to cool the soaring cost of living, Turkey’s central bank increased its interest rate to 50%; this compares to a rate of 8.5% just a year ago.

The pan-European Stoxx 600 index reached a record high on 13 March boosted by upbeat company results from the likes of energy supplier E.ON and retailer Zalando. Buoyant company forecasts indicate that businesses are feeling optimistic about the future.

US

Inflation in the US unexpectedly increased to 3.2% in the 12 months to February 2024. The news dampened hopes that an interest rate cut would be announced soon.

A consumer sentiment index from the University of Michigan suggests Americans have a gloomy outlook about economic conditions and prospects for the future. Pessimistic consumers might be more likely to curb their spending, which could harm businesses.

Data from the US Federal Reserve also indicates that businesses are taking a more cautious approach. Average hourly earnings increased by just 0.1% in February 2024, while unemployment reached 3.9% – the highest figure since January 2022.

Technology giant Apple saw its shares fall by around 2.5%, wiping around $70 billion (£55 billion) off the value of the company, on 4 March following an EU-issued fine. The EU fined the company €1.8 billion (£1.54 billion) after it was found to have broken competition laws by imposing curbs on app developers.

Asia

Japan’s main index, the Nikkei, hit 40,000 points for the first time on 4 March after it increased by 0.5%, partly thanks to a weak Japanese Yen helping exporting businesses. The milestone follows a strong start to the year – the Nikkei has gained almost 20% since the start of 2024 thanks to booming technology firms.

The Bank of Japan also made its first interest rate hike in 17 years and ended eight years of negative interest rates, which sought to encourage lending. The bank’s base rate increased from -0.1% to 0.1% after board members said they expected to achieve 2% inflation in the coming year after decades of deflation and stagflation.

China continues to face a property crisis, which is affecting consumer spending and lending, as well as economic growth.

The Chinese government previously cracked down on property speculation that sent prices soaring. However, the property market peaked in 2020 and has faced a downturn ever since.

According to the country’s National Bureau of Statistics, house prices continued to fall in major cities in February. The organisation said it expects real estate to remain the main drag on economic growth in 2024.

Please note:

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested.

Past performance is not a reliable indicator of future performance.

Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

How financial protection could offer security to parents

As a parent, your child facing an illness could affect your finances just as much as becoming ill yourself. Appropriate financial protection could offer you a safety net when you need it most, including if you need to take a long period off work to care for your child.

Read on to find out how financial protection could offer parents peace of mind and financial security if the worst should happen.

Financial protection could pay out a lump sum if your child is diagnosed with a critical illness

No parent wants to think about their child being diagnosed with a serious illness, but, while rare, it does happen.

Reviewing whether critical illness cover could provide security for your family now means that if your child suffers an illness you can focus on them, rather than worrying about your finances.

Critical illness cover pays out a lump sum if you’re diagnosed with a covered illness. If your child is diagnosed, it will usually pay out a proportion of the full amount, such as 50%. This financial safety net could mean you’re able to take time off work to care for your child or spend it enjoying time with your family.

Critical illness cover might also come with other benefits that would be valuable for your family, such as:

- Lump sum payout if your child is hospitalised following an accident

- Accommodation payments so you’re able to stay close to your child if they’re in hospital

- Childcare costs if you’re diagnosed with a critical illness.

The cost of critical illness cover will depend on the potential payout you want, as well as factors like your age and health. If you don’t pay the premiums, your cover will lapse.

Often, children will be added to your critical illness cover automatically. However, for some providers, you may need to contact them, and your premiums could rise as a result.

Your children will typically be covered from when they are a few weeks old until they’re 18, or 21 if they’re in full-time education. This can vary between providers, so it’s important to check the details when comparing options.

There might be other restrictions you need to be aware of. For example, some forms of cover will allow only one claim per child or may exclude conditions that are present at birth.

Private medical insurance could also put your mind at ease

While you’re considering taking out financial protection that would pay out if your child is diagnosed with a serious illness, you might also want to think about private medical insurance.

According to a BBC report, waiting times and staff shortages have led to public satisfaction in the NHS falling. In fact, just 24% of people polled said they were satisfied with the NHS in 2023.

If you’re worried about accessing services through the NHS, private medical insurance could offer you peace of mind. It could cut down waiting times for a range of services, such as tests and consultations, as well as more choice when deciding where your family receives treatment.

If you or your child needed to stay in a hospital, private medical insurance could also cover the cost of a private room to give you more privacy.

It’s not just physical illnesses that private medical insurance might cover either. Some providers could also give you access to mental health services, which may be valuable for your child.

Indeed, Aviva reported that the number of children and young people seeking support for their mental health increased by 25% in 2023 when compared to just a year earlier.

The cost of private medical insurance will depend on a range of factors, including who is covered, your lifestyle, and family medical history. The level of cover can vary. So, taking the time to understand how comprehensive cover is and any exclusions that might affect your family could help you choose an option that’s right for you.

Contact us if you’d like to discuss how you could prepare for the unexpected

Taking out appropriate financial protection is just one way you could prepare for the unexpected and protect your family. If you’d like to talk to us about how you could update your financial plan to reflect your priorities, please contact us.

Please note:

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

Note that financial protection plans typically have no cash in value at any time and cover will cease at the end of the term. If premiums stop, then cover will lapse.

Cover is subject to terms and conditions and may have exclusions. Definitions of illnesses vary from product provider and will be explained within the policy documentation.

3 valuable ways business owners could extract profits

As a business owner, deciding how to extract profits from your firm could be a crucial decision. It may affect your tax liability and that of your company. Read on to understand three essential ways you could take money from your business and potential tax implications you might want to weigh up before deciding which is the right route for you.

Many business owners will use a combination of the three options below to extract profit from their business to fund their day-to-day expenses and create long-term financial security.

1. Taking a salary

An obvious way to access profit from your business is to pay yourself a salary.

Paying yourself a salary from your business could help ensure you have a regular income to cover day-to-day expenses. A reliable income source could also make some situations more straightforward, such as applying for a mortgage. So, you might want to consider your short- and medium-term plans when deciding your salary.

In addition, you may also factor in how your salary could affect your tax liability. Your salary could be liable for Income Tax in the same way as other employees.

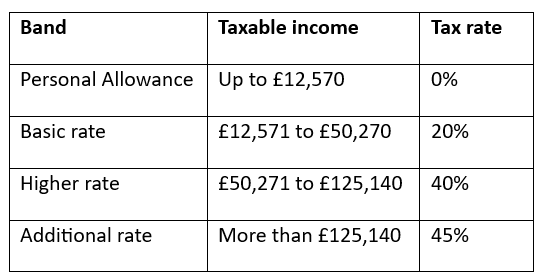

For the 2024/25 tax year, the Income Tax bands and rates are:

Income Tax allowances and rates are different in Scotland

Being mindful of the Income Tax thresholds might help you to manage your finances and avoid an unexpected bill.

As well as Income Tax, there could be other taxes and allowances you factor in. For instance, moving into a higher tax bracket could reduce your Personal Savings Allowance and lead to you paying tax on the interest your savings earn. In addition, high earners could be affected by the Tapered Annual Allowance, which reduces the amount you can tax-efficiently contribute to your pension.

If you would like to talk about the implications of your Income Tax bracket when setting your salary, please contact us.

2. Supplementing your income with dividends

Dividends could be a tax-efficient way to boost your salary. They provide a way to distribute company profits among its shareholders. So, when your business is doing well, dividends could supplement your other sources of income.

In 2024/25, the Dividend Allowance means you can take dividends up to £500 before tax is due. This allowance has fallen in recent years – it was £2,000 in 2022/23. So, if you’re a business owner who uses dividends to extract profits and haven’t reviewed your tax liability recently it could be a worthwhile task.

Dividends could prove valuable even if you exceed the Dividend Allowance due to the tax rate likely being lower than the rate of Income Tax.

The rate of tax you pay will depend on which Income Tax band(s) the dividends that exceed the allowance fall within once your other income is considered. For 2024/25, the Dividend Tax rates are:

- Basic rate: 8.75%

- Higher rate: 33.75%

- Additional rate: 39.35%

It’s not possible to carry forward your Dividend Allowance if you don’t use it in the current tax year. So, making dividends a regular part of your income could be useful.

3. Making pension contributions

Making pension contributions could help secure your long-term finances. This is because a pension is a tax-efficient way to save for your retirement – the investment returns held in a pension aren’t liable for Capital Gains Tax.

In addition, your contributions benefit from tax relief at the highest rate of Income Tax you pay. So, if you’re a basic-rate taxpayer who wants to top-up your pension by £1,000, you’d only need to deposit £800.

Usually, your pension provider will automatically claim tax relief at the basic rate on your behalf. However, if you’re a higher- or additional-rate taxpayer, you’ll need to complete a self-assessment tax return to claim the full amount you’re eligible for.

As well as contributions from your salary, you can set up employer contributions from your business to support your retirement goals.

In 2024/25, the pension Annual Allowance is £60,000. This is the maximum you can pay into your pension while retaining tax relief. However, you can only claim tax relief on 100% of your annual earnings. All contributions count towards your Annual Allowance, including employer contributions and those made by other third parties.

Remember, you can’t usually access your pension until you’re 55 (rising to 57 in 2028). So, if you’re using pension contributions to extract profits from your business you may want to consider when you’ll want to access the money and your long-term plans.

Extracting profits tax-efficiently could reduce your business’s Corporation Tax bill

As well as your personal finances, you may want to incorporate your business’s tax liability when deciding how to extract profits.

Corporation Tax is paid on the profits you make, and some outgoings are allowable expenses that could be deducted during your calculations. Allowable expenses may cover employee salaries, including your own, and pension contributions. In addition, employer pension contributions are deducted before employer National Insurance is calculated.

If your company makes more than £250,000 profit during a tax year, you’ll usually pay the main rate of Corporation Tax, which is 25% in 2024/25. If your company made a profit of £50,000 or less, then you’ll pay the “small profits rate”, which is 19% in 2024/25.

You may be entitled to “marginal relief” if your profits are between £50,000 and £250,000. The relief provides a gradual increase in the Corporation Tax rate between the small profits rate and the main rate.

Keeping these thresholds in mind when you’re extracting profits from your business could help you make decisions that are tax-efficient for both you and your company.

Contact us to talk about your personal finances

As a business owner, your personal finances might be more complex. We could offer support and create a tax-efficient financial plan that reflects your circumstances and long-term goals, including your business exit strategy. Please contact us to arrange a meeting to discuss how we can help you.

Please note:

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

The Financial Conduct Authority does not regulate tax planning.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.

Could you face an unexpected bill now the Capital Gains Tax allowance has halved?

The gains you can make before potentially paying Capital Gains Tax (CGT) have halved for the 2024/25 tax year. If you plan to dispose of assets, the change could affect you. Read on to find out when you could be liable for CGT and some steps you might take to manage a bill.

CGT is a tax on the profit you make when you sell certain assets that have increased in value. CGT could be due when disposing of a range of assets, including:

- Shares that aren’t held in a tax-efficient wrapper

- Property that isn’t your main home

- Personal possessions that are worth £6,000 or more, excluding your car.

The amount of profit you can make during the year before CGT is due has fallen significantly over the last couple of years.

The Annual Exempt Amount has fallen to £3,000 in 2024/25

According to research from the University of Warwick, less than 3% of UK adults paid CGT in the decade to 2020. In fact, in any given year, just 0.5% of adults were liable for CGT. Yet, the total amount paid through CGT tripled between 2010 and 2020 to £65 billion.

The government has substantially reduced the amount of profit you can make before CGT is due, so the number of people paying the tax could soar over the coming years.

In 2022/23, the amount you could make before CGT was due, known as the “Annual Exempt Amount”, was £12,300. This was reduced to £6,000 in 2023/24, and from 6 April 2024, it is reduced further to just £3,000.

If your total profits during the tax year exceed the Annual Exempt Amount, your CGT bill will depend on which tax band(s) the taxable gains fall into when added to your other income. In 2024/25, if you’re a:

- Higher- or additional-rate taxpayer, your CGT rate will be 20% (24% on gains from residential property)

- Basic-rate taxpayer, you may benefit from a lower CGT rate of 10% (18% on gains on residential property) if the taxable amount falls within the basic-rate Income Tax band.

So, if you have assets to sell, considering how to mitigate a potential bill could be valuable.

6 practical ways you could reduce your Capital Gains Tax bill

1. Time the sale of your assets

The Annual Exempt Amount cannot be carried forward to a new tax year if you don’t use it. Timing the disposal of your assets could help you make use of the allowance to minimise your bill. For instance, you might hold off selling an asset until a new tax year starts if you’ve already exceeded the Annual Exempt Amount in the current year.

2. Pass assets to your spouse or civil partner

The Annual Exempt Amount is an individual allowance, and you can pass assets to your spouse or civil partner without tax implications. So, if you’ve used your Annual Exempt Amount, transferring an asset to your partner before you dispose of it to use their allowance might be an option you want to consider.

3. Use your ISA to invest tax-efficiently

An ISA is a tax-efficient wrapper for saving or investing. Returns and profits made on investments held in an ISA are not liable for CGT. So, if you want to invest, choosing an ISA may help you mitigate a tax bill.

If you already hold investments outside of an ISA, you could sell the investments and immediately buy them back within your ISA. This strategy of moving your investments to a tax-efficient account is known as “Bed and ISA”.

In the 2024/25 tax year, you can add up to £20,000 to ISAs.

4. Use a pension for long-term investments

Like ISAs, pensions offer a tax-efficient way to invest – investments held in a pension are not liable for CGT.

In the 2024/25 tax year, the pension Annual Allowance is £60,000 for most people. This is the maximum amount you can pay into your pension during the tax year while still benefiting from tax relief. However, you can only claim tax relief on up to 100% of your annual earnings.

If you’ve already taken an income from your pension or are a high earner, your Annual Allowance could be as low as £10,000. If you’re not sure what your Annual Allowance is, please contact us.

The Annual Allowance can be carried forward for up to three tax years. So, if you’ve used all your Annual Allowance in 2024/25, you may want to review your pension contribution in previous tax years.

Before you boost your pension, considering your investment goals and time frame might be essential. You cannot usually access the money in your pension until you’re 55, rising to 57 in 2028, so it isn’t the right option for everyone.

5. Manage your taxable income

As mentioned above, basic-rate taxpayers may benefit from a lower rate of CGT if the gains fall within the basic-rate tax band. As a result, managing your taxable income to stay below Income Tax thresholds once expected profits are included could slash a CGT bill.

6. Deduct losses from your gains

It is possible to deduct losses from the profits you make. You must report the losses to HMRC by including them on your tax return. When you report a loss, the amount is deducted from the gains you make in the same tax year.

If your total taxable gain is still above the tax-free allowance, you can deduct unused losses from previous tax years. If the losses reduce your gain to the tax-free allowance, you can carry forward the remaining losses to a future tax year.

Contact us to talk about your tax liability

Whether you’d like to understand how you could reduce a potential CGT bill or you want to review your financial plan with tax efficiency in mind, please contact us. We could help you identify ways to cut your tax bill in 2024/25 and beyond.

Please note:

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested.

Past performance is not a reliable indicator of future performance.

Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.

The Financial Conduct Authority does not regulate tax planning.

More retirees may need to consider tax liability as State Pension nears the Personal Allowance

Pensioners have benefited from an 8.5% increase in the State Pension. While the boost is likely to be welcomed by many, the full new State Pension is nearing the Personal Allowance threshold. As a result, some retirees might need to consider their Income Tax liability for the first time or could be pushed into a higher tax bracket.

The full new State Pension is £221.20 a week in 2024/25

Under the triple lock, the State Pension increases each tax year by the highest of the following three measures:

- Average wage growth

- Inflation

- 2.5%

The triple lock plays an important role in preserving the spending power of pensioners. If your State Pension income remained the same throughout retirement, it would gradually buy less as the cost of goods and services increased. As you could claim the State Pension for several decades, the triple lock might play an essential role in maintaining your lifestyle.

For 2024/25, the full new State Pension increased by 8.5% (the average wage growth measure) to £221.20 a week, or £11,502 a year.

To be entitled to the new full State Pension, you need at least 35 qualifying years of National Insurance contributions or credits. If you have fewer qualifying years, you’ll usually receive a portion of the full State Pension but you still benefit from the triple lock.

If you reached the State Pension Age before 6 April 2016, your State Pension is based on the old rules that existed at that time. You might receive a lower amount if you were contracted out of the Additional State Pension.

You can use the government’s State Pension forecast if you’d like to understand how much you could receive through the State Pension and when you can claim it.

Frozen allowances could mean your tax bill increases in retirement

The government has frozen key Income Tax thresholds at 2021/22 levels until April 2028. As a result, more people are expected to pay Income Tax in the coming years as wages and the value of benefits such as the State Pension rise.

Indeed, the Office for Budget Responsibility (OBR) predicts the freeze will lead to 3.2 million new taxpayers and 2.1 million new higher-rate taxpayers by 2027/28. It’s not just an issue for workers – it could affect retirees too.

The Personal Allowance – the amount of income you can earn before tax is usually due – is £12,570 in the 2024/25 tax year, and it’s expected to remain at this level until 2028.

The latest rise under the triple lock means most of your Personal Allowance could be used by the State Pension if you’re entitled to the full amount. You’d only need to receive around £90 a month from other sources before you become liable for Income Tax. As a result, some people who haven’t paid Income Tax since retiring could now face an unexpected bill.

Similarly, the tax thresholds for paying the higher and additional rate of Income Tax are frozen until 2028. So, even if your income from other sources doesn’t increase, you could find yourself in a higher tax bracket due to the State Pension rise.

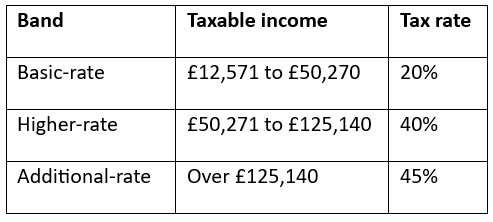

For 2024/25, the Income Tax bands are:

How to manage your tax liability in retirement

To manage your tax liability in retirement, one of the first steps is to track your income – are you nearing any thresholds that could lead to a higher bill than expected?

You might have several different income streams you need to consider, such as the State Pension, annuities, or flexible withdrawals from your pension.

Once you’ve set out your income, you can start to create a tax strategy that suits your needs.

For instance, you can usually take up to 25% of your pension as a tax-free lump sum (for most people this will be capped at a maximum of £268,275 in 2024/25), which you may spread across multiple withdrawals. This could be a useful way to access large amounts without increasing your tax bill. However, once you exceed the tax-free amount, the money you withdraw as a lump sum would usually be added to your other taxable income and could be taxed.

As a retiree, you may be in control of your income sources and could adjust them to reduce your tax liability. For example, if you take an income from your pension using flexi-access drawdown, you might choose to lower the amount so you remain below an Income Tax threshold.

You might also choose to supplement your income from other tax-efficient sources, like an ISA. An ISA offers a tax-efficient way to save and invest, so you might make withdrawals to support your day-to-day costs without increasing your tax liability.

Contact us to talk about how to improve your tax efficiency in retirement

If you’d like to understand what steps you could take to improve tax efficiency in retirement, we could help. We’ll take the time to understand your goals, lifestyle, and assets and then work with you to create a retirement plan that’s tailored to you. Please contact us to arrange a meeting.

Please note:

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.

What you need to know about taking your pension tax-free lump sum in 2024/25

Taking a tax-free lump sum from your pension could be a fantastic way to kickstart your retirement plans. If it’s something you’re thinking about, it’s important to consider the long-term implications and understand how much you could withdraw from your pension before facing a tax bill, as the rules have changed in 2024/25.

Previously, you could take up to 25% of your pension as a tax-free lump sum. This could be through a single withdrawal or spread across several. However, following the removal of the pension Lifetime Allowance, there is now a cap.

The “Lump Sum Allowance” is £268,275 in 2024/25

In 2023, chancellor Jeremy Hunt announced the pension Lifetime Allowance (LTA) would be scrapped in the 2024/25 tax year. The LTA limited the amount of pension benefits you could build up during your lifetime without incurring an additional tax charge.

With workers now able to save more into their pension tax-efficiently during their careers, the government has frozen the limit on tax-free withdrawals from your pension.

In 2024/25, you can still usually take up to 25% of your pension tax-free – although now there is a cap on the total tax-free cash you can take. This is the new Lump Sum Allowance (LSA) of £268,275.

Your LSA may be higher if you benefit from one of the various types of LTA “protection”, such as “individual” or “fixed” protection.

Withdrawing a tax-free lump sum could harm your long-term finances

If you want to take a lump sum from your pension, the new rules aren’t the only area you might want to consider. You may also want to weigh up the effect it could have on your long-term finances.

There are plenty of reasons why you may want to take a lump sum from your pension, and some could improve your financial position in retirement. For example, you could use the lump sum to clear your mortgage or other debt, which may significantly reduce your outgoings in retirement and lead to a more comfortable and secure lifestyle.

Alternatively, you might plan to use the money to reach aspirations, like travelling the world once you stop working.

It could be a great way to fund your early retirement plans. However, taking a lump sum from your pension could have a significant effect on your long-term financial security and income. Not only will you be reducing the size of your pension but, as your pension is usually invested, you may have a smaller pot left to invest, reducing your potential for further growth.

Understanding the potential implications of taking a lump sum at the start or during your retirement could help you make a decision that’s right for you.

You may find that after taking a lump sum from your pension you’ll still be financially secure and able to reach long-term goals. If this is the result, you might feel more confident taking a lump sum and more able to enjoy your retirement.

On the other hand, if you find taking a lump sum could harm your long-term finances, you may decide to halt your plans or make adjustments to improve your financial security throughout retirement.

As a financial planner, we can help you understand what the consequences of taking a lump sum could mean for you.

On average, over-55s spend a third of their tax-free lump sum within 6 months

A 2023 survey from Standard Life found that over-55s who have taken a tax-free lump sum, on average, spend or expect to spend a third of their withdrawal within six months.

While having some cash to fall back on in retirement could be useful, withdrawing a lump sum to hold the money outside of your pension might not be financially savvy.

The money held in your pension is usually invested, so it has the potential to deliver returns during your retirement. In addition, investments held in your pension are not liable for Capital Gains Tax, so it provides a tax-efficient way to invest. If you withdraw money from your pension to hold in cash, its value could fall in real terms and you might miss out on potential long-term growth.

Of course, investment returns cannot be guaranteed and they could experience volatility. As a result, it’s important to consider your risk profile and circumstances when deciding how to manage your pension.

Setting out how you plan to use your tax-free lump sum and making it part of your wider financial plan could help you assess if withdrawing it now or in the future is right for you.

Contact us to talk about your pension withdrawals

When you’re accessing your pension, whether to take a lump sum or a regular income, you might worry about what’s right for you. Working with a financial planner could give you confidence in retirement. Please contact us to talk to one of our team about how to access your pension in a way that’s tax-efficient and aligns with your goals.

Please note:

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

Recent Comments